[Click on image for larger version]

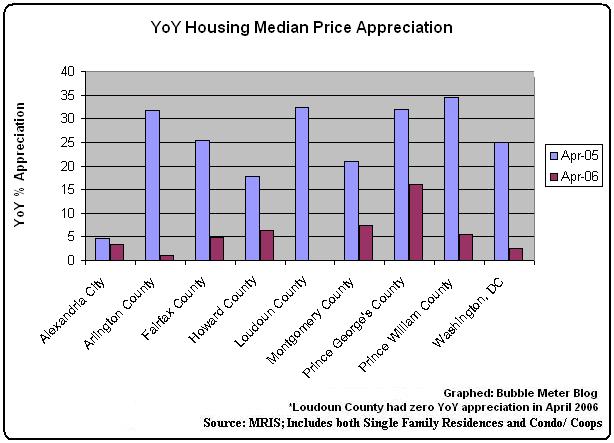

Notice how in some of the locales the year over year (YoY) price 'appreciation' for April 2006 is less then inflation. In these locales, real dollar price declines are a reality.

Bubble Meter is a national housing bubble blog dedicated to tracking the continuing decline of the housing bubble throughout the USA. It is a long and slow decline. Housing prices were simply unsustainable. National housing bubble coverage. Please join in the discussion.

Why don't you chart the median month by month, that way we can see clearly what a "soft landing" looks like?

ReplyDeleteanon,

ReplyDeleteHere it is:

http://novabubble.blogspot.com/2006/04/march-2006-nvar-statistics-are-out.html

holy smokes, somebody really put some hours into that. Thanks for that David.

ReplyDeleteDavid,

ReplyDeleteWhy can't you post real numbers on this "bubble" theory of yours.

;)

My $0.02.

"In these locales, real dollar price declines are a reality."

ReplyDeleteNot really. Housing costs are one of the things measured in inflation. In any event, that appears only to be Arlington County.

Sorry the numbers, once again, contradict everybody's claims that prices are falling. They are, in fact, rising, as this data makes perfectly clear.

"Housing costs are one of the things measured in inflation."

ReplyDeleteNot in the CPI. They measure rents.

" In any event, that appears only to be Arlington County. "

Arlington, Alexandria, Louduon and DC.

"They are, in fact, rising, as this data makes perfectly clear."

These are YoY. Wait a few more months. Then look at the YoY

"Sorry the numbers, once again, contradict everybody's claims that prices are falling."

ReplyDeleteIf you want to compare March to April lets look at Louduon county.

March 2006 Median: 503,500

April 2006 Median: 470,000

What's that a 6% decline in one month?

Nice try anon.

And look where it's highest... Prince George's County, which had a record number of homicides last year (yes, more than in any one of the crack epidemic years).

ReplyDeleteA Redskins fan

David, you choose one set of number to prove one thing, and another to prove another point. You're getting to be as bad as some of the idiot realtors on here. This blog jumped the shark when it started to focus on U.S. macro-economic trends while at the same time displaying a total ignorance of the mortgage finance market, and got away from what it did best--discuss local, observable anecdotes about the decline in the real estate market.

ReplyDelete"Sorry the numbers, once again, contradict everybody's claims that prices are falling."

ReplyDeleteDon't forget this is appreciation from (2005 to 2006). The price declines did not occur until recently. Yes this graph does not show prices are falling, but there is plenty of other data to support this. Just wait until 2007 YoY appreciation charts come out.

"March 2006 Median: 503,500

ReplyDeleteApril 2006 Median: 470,000

What's that a 6% decline in one month?

Nice try anon. "

Maybe you should close up shop here and open a Loudon County blog, because your DC blog isn't working out.

"The price declines did not occur until recently. Yes this graph does not show prices are falling, but there is plenty of other data to support this. Just wait until 2007 YoY appreciation charts come out.

ReplyDelete"

Ah, so they're secret invisible price declines. That would explain it. Thanks for clearing that up.

"

ReplyDeleteArlington, Alexandria, Louduon and DC."

I guess in David land, inflation is like 10%. You're right, I missed Louduon, but Alexandria is above the rate of inflation, while DC is at about the rate or a tick above it.

"These are YoY. Wait a few more months. Then look at the YoY "

Yeah, I'm sure. One of these days, future data are going to vindicate you. But today is yet another dark day in the "life" of a bubble blogger.

"What's that a 6% decline in one month?"

ReplyDeleteBy the way, are these the same houses that were sold in April as in March, or are they different houses. Because that might explain why they sold for different prices. I'm sure you know that the median price ticked up in DC month over month.

How much does the median need to rise from where it is now in order to reach the high set last summer?

ReplyDelete"Maybe you should close up shop here and open a Loudon County blog, because your DC blog isn't working out."

ReplyDeleteIt is a national housing blog. It has a particular focus on the DC metropolitan area blog.

"By the way, are these the same houses that were sold in April as in March, or are they different houses. Because that might explain why they sold for different prices. I'm sure you know that the median price ticked up in DC month over month."

This is how the housing industrial complex and the media reports. There are admittingly problems with this approach. But the dramatic change in YOY is telling.

"I guess in David land, inflation is like 10%. You're right, I missed Louduon, but Alexandria is above the rate of inflation, while DC is at about the rate or a tick above it."

ReplyDeleteinflation is about 4%

"got away from what it did best--discuss local, observable anecdotes about the decline in the real estate market."

ReplyDeleteDavid - I agree with this blogger. For national news, I go to another blog, and come here for local perspective. I think since your blog tried to become something else, it's loosing its personality.

"This blog jumped the shark when it started to focus on U.S. macro-economic trends while at the same time displaying a total ignorance of the mortgage finance market"

ReplyDeleteGive me an example of how "total ignorance of the mortgage finance market"?

"This is how the housing industrial complex and the media reports. There are admittingly problems with this approach. But the dramatic change in YOY is telling. "

ReplyDeleteYeah, it's telling me that prices are still going up. PWN3D.

I don't think that comparing price increases to inflation is really fair. Let's take my example. A few years ago I bought a house for $130k. The mortgage on it was about $1000 per month - about the same as rent. Let's assume I got 3% price increase in a year. The house is now worth $3900 more. Sure, the real value fell but from my perspective I went from maybe $10k in equity to $13.9k not including some minor equity from the mortgage payments. That's not bad for a $10k investment. Sure, the interest is higher than the increase in value but that's not a big deal since the alternative is rent.

ReplyDeleteWith all that said, I'm a huge bubble believer. I just don't think I will get excited until we have real YoY declines (and we will).

And, yes, I know that rent is no longer anywhere near mortgage payments (or interest payments) so that does alter the argument but my point is merely that you can't simply say it's bad for a homeowner when price increases < inflation.

David - I'm sure you know this, but the deniers are complaining and objecting only because your blog is effective in spreading the truth about the housing bubble. I suspect they may still be under contract for some pre-construction condos. My view is that the more the deniers protest the more we should turn up the heat.

ReplyDeleteI agree with Tom that putting 06 on the right side of 05 might be better (if its not too much work). Then the bars will be in declining order like a downward slope.

Keep up the great work. I really enjoy your blog. You are doing your readers a great service.

John,

ReplyDeleteDo you rent in Clarendon? How much do you pay per month to live in that place?

bryce

John,

ReplyDeleteThanks for your support.

"I agree with Tom that putting 06 on the right side of 05 might be better (if its not too much work). Then the bars will be in declining order like a downward slope."

Changed. Fixed.

"I'm sure you know this, but the deniers are complaining and objecting only because your blog is effective in spreading the truth about the housing bubble."

AMEN! I concur.

"My view is that the more the deniers protest the more we should turn up the heat."

I have been truning up the heat with my recent posts. :-)

David

>I went from maybe $10k in equity to $13.9k not including some minor equity from the mortgage payments.That's not bad for a $10k investment.

ReplyDeleteThe underlying investment theory that you use here is leverage - you got 3.9K for a 10K investment (and 120K borrowed).

Let's set apart for a moment the fact that if you gained only 3%, and inflation was 4%, it was a loss in real terms.

Your equity came at a price. You think you got 3.9K on 10K. Not really. If you paid more as 'cost of money' for your investment, it is a loss.

This can easily demonstrated by the extreme example - If you take a 100% I/O loan, then you get 3.9K equity for nothing. Huh? However you paid 12000 as interest - that was the cost of money.

In your case, you are saying this cost is zero, as its equal to the rent you paid. So in _that_ case it makes sense. Your net cost of money is zero.

Financial theory states that for a leveraged investment to be positive,

"the assets in which borrowed funds are invested must earn a rate of return greater than the fixed rate required by fund suppliers"

Or in other words, if you want a profit, your investement must appreciate at a rate higher than the effective rate at which you borrowed to invest in it.

bibba,

ReplyDeleteCan you run the numbers again and factor in some tax deduction benefits this time? I'm guessing that the buyer might deduct his or her mortgage interest on their tax return and thus reduce their taxable income by a favorable amount. Perhaps not, but that is was most people seem to do these days...

bryce.

Seems like there's a few people out there who are pretty scared right now. I guess they must be realizing that they are screwed.

ReplyDeleteYou have to have your head pretty far up your a$$ not to see what's going on. Charts and graphs are nice but the real story are all the streets with 50% of the houses for sale and no one looking and all the condos with open house after open house that no one is attending.

This blog is not why things are turning. The market is turning because it long ago departed from fundamentals.

>Can you run the numbers again and factor in some tax deduction benefits this time?

ReplyDeleteUnfortnately, I dont have an excel spdsht. right now. An easy and dirty way to do this would be to take your net expense as the cost of money

i.e

cost of money/yr = yrly interest - (rent + tax deduction)

From this yrly interest, back calculate your _effective_ interest rate.

Of course, one should include the prop tax and maint and caluclate investment expense, rather than cost of money alone, if one is really looking at profit.

And if you want to be more accurate, you should calculate for every year - since yrly interest (if ARM), rent and other factors change. But even without this, a quick and dirty calculation with investemnt expense will give you the rough numbers.

I think any housing calculator on the Web will give you a quick number. (Though mind the inflation and returns rate assumptions used in those - relative changes in those rates can change net results dramatically)

What I wanted to point out is that leverage is not free.

The people who are making fun of this blog because prices have still gone up YoY are clueless. You guys must have master degrees in cluelessness, with a bachelors degree in stupidity and a minor in reading tarot cards.

ReplyDeleteAnybody with at least one analytical brain cell would take a look at the dramatic change in YoY numbers for 2005 and 2006, and wonder how the prices have changed recently in month over month (MoM). The median sales prices have gone down MoM in many locales.

What are you guys going to say when we get to September and the YoY numbers are down for several of these counties, which looks like almost a 100% certainty at this point?

David, you are doing a great job in presenting all of this data. Much of it is very compelling and hard to ignore.

P.S.: If any of you investors get over your heads on a property, post it on this blog. I may get in contact with you on possible remedies. (Not joking here.)

"What are you guys going to say when we get to September and the YoY numbers are down for several of these counties, which looks like almost a 100% certainty at this point?"

ReplyDeleteKeep loving having lots of money and making fun of people like you who populate blogs dedicated to reveling on the misery of others.

please remove the anonymous post dated May 11, 2006 6:33 PM => it points to a porn site.

ReplyDelete"David, you are doing a great job in presenting all of this data. Much of it is very compelling and hard to ignore."

ReplyDeleteThank YOU. :-)

Revel in the misery of others? I actually own a house, and I don't find it funny that people are getting screwed. It's pretty sad actually. If you don't think I should be stating what I think will be true in 4 months, that's just too bad.

ReplyDeleteMan oh man, the new flippers in these areas are about a half step away from becoming a "bubble bitch" to some mortgage bank (owing more than the house is valued)! A great time to be on the sidelines watching the ass-pounding given to the flippers begin in earnest! Pass the popcorn please!

ReplyDeleteDavid - I'm sure you know this, but the deniers are complaining and objecting only because your blog is effective in spreading the truth about the housing bubble. I suspect they may still be under contract for some pre-construction condos. My view is that the more the deniers protest the more we should turn up the heat.

ReplyDeleteI agree with Tom that putting 06 on the right side of 05 might be better (if its not too much work). Then the bars will be in declining order like a downward slope.

Keep up the great work. I really enjoy your blog. You are doing your readers a great service.