- Short Term Interest = Small Increase

- 30 Year Fixed Mortgages = Small Increase

- Foreclosures = Small Increase

- Lending Standards = Small Increase

- Gasoline Prices = Small Increase

- Bubble Cheerleading = Small Decrease

- Housing Inventory = Large Increase ( added)

- Housing Prices = Small Decrease

- Flipper's Happiness = Large Decrease

Wednesday, August 31, 2005

The Next Four Months

Here is how I expect things to happen in the next four months:

Jerry Howard: There is no housing bubble

It's big box office this summer in the national media, but paraphrasing Mark Twain, reports of an impending housing price collapse are greatly exaggerated.Who is Jerry Howard? Jerry Howard is executive vice president and CEO of the National Association of Home Builders.

Demographic and economic fundamentals support today's housing expansion.

To begin with, strong household formations, fueled by population growth and immigration, are pushing average annual demand for new housing into the 2 million-unit range for the decade ahead, about today's production level. Equally important, the U.S. economy is fueling enough new jobs and income gains to support brisk housing demand even as interest rates inch upward.

Second, the unusually steep price gains provoking much of the speculation over a housing bubble are mainly in California, Nevada, Florida and the Northeast corridor, and aren't the norm for most local markets.

Third, builders are running into serious obstacles, such as excessive growth controls or moratoria, in lining up land for development in the fastest growing housing markets. In the face of unrelenting housing demand, this is making housing shortages even worse, increasing the cost of building and persistently increasing house prices.

Fourth, unlike trading in stocks and bonds, buying a home is a costly and time-consuming process that is not susceptible to the kind of run on the market that occurred in the dot.com collapse. Also, the vast majority of families live in the homes they buy for a long time and don't flip them for a profit after a few months.

Finally, history shows that most unsustainable house price booms end quietly, as house price appreciation slows while ongoing increases in household income and housing supply help restore balance to local markets. A recent Federal Deposit Insurance Corp. study shows that house price booms lead to price busts only when local economies stumble for other reasons, such as a national recession. With the U.S. economy in the midst of a strong expansion, those risks are quite low for the foreseeable future.

It doesn't take a Ph.D. in economics to conclude that short supply and high demand do not add up to a housing bubble.

Tuesday, August 30, 2005

Housing Bubble Paraphanelia

About a week ago I ordered the Mr. Housing Bubble T-Shirt. But more significantly, my boss ordered for me the Mr. Housing Bubble Mousepad. I was thrilled. :-) In the office my nickname is Bubble Boy.

Fla.: FBI Says Mortgage Fraud High in the State

Here is a NAR article titled Fla.: FBI Says Mortgage Fraud High in the State

A new Financial Crimes Report from the FBI has named Florida one the nation's top 10 hot spots for mortgage fraud. The report states that such fraud is "pervasive and growing" in the state.

The most common violations include overpriced appraisals, property flipping (purchasing a home to resell at a higher price in a short time frame), and equity skimming (using a quit claim deed to sign a property over to an investor who never pays for the property).

Lydia Pisano, president of the Orlando Regional REALTORS® Association and a team leader with Keller Williams Homestead Realty in Orlando, says mortgage fraud is definitely a growing problem in the state. She credits the hot housing market with creating a breeding ground for the fraud, particularly when it comes to inflated appraisals.

"Sellers are asking a lot more for their homes than they are worth, and now we're seeing homes not appraising and price reductions," Pisano says. She adds that the trend has led lenders to tighten their review processes and to kick back inflated appraisals as unacceptable.

Pisano says some mortgage companies also are guilty of activities or carelessness that can lead to fraud. For example, "The buyers tell the mortgage company that they make $300,000 a year, and no one ever checks it," says Pisano.

Other states cited by the report as high in mortgage fraud include Georgia, South Carolina, California, Illinois, Michigan, Utah, Missouri, Nevada, and Colorado.

Homebuilders' Stock Prices Continue to Fall

Homebuilders' stocks continue to tumble. The market knows what is coming. The bubble is about to burst.

Monday, August 29, 2005

Wise Comments

Merrill Lynch economists Kathleen Bostjancic and David Rosenberg said in a economic commentary:

"We find that the red-hot housing sector alone, which typically represents just 5% of the total economy, accounted for an astounding 50% of the overall growth in the U.S. economy by the first half of this year, and more than half of the private payroll jobs created since fall 2001 were in housing-related sectors,"

"We argue this represents an unhealthy and disproportionate share of economic growth. The overreliance on residential investment leaves the economy very vulnerable if housing demand and prices cool -- prices do not need to even fall; just a slowing in the pace of home price appreciation would have a noticeable negative impact on economic growth -- not unlike the fallout following the frenzied tech overinvestment in the late 1990s."

Sunday, August 28, 2005

Shame on Lereah

David Lereah the chief economist ( cheerleader) for the National Association of Realtors had this to say to the LATimes:

Wait a second. Let's say interest rates stay at 5.8% and you take out a home equity loan or don't pay off you mortgage, then those borrowed dollars are costing you about 4.5% ( adjusted for tax breaks). If you keep the money under your mattress then it is costing you the price of inflation per year. It is clearly not the same. Shame on Lereah.

"If you paid your mortgage off, it means you probably did not manage your funds efficiently over the years. It's as if you had 500,000 dollar bills stuffed in your mattress."

Wait a second. Let's say interest rates stay at 5.8% and you take out a home equity loan or don't pay off you mortgage, then those borrowed dollars are costing you about 4.5% ( adjusted for tax breaks). If you keep the money under your mattress then it is costing you the price of inflation per year. It is clearly not the same. Shame on Lereah.

Saturday, August 27, 2005

Meet Doug Duncan

Doug Duncan is the chief economist for the Mortgage Bankers Association. He is indeed a bubble cheerleader. Below are some of his quotes

The existing home sales numbers "give me some reason to believe that we may be starting to see the slowing take place," said Doug Duncan, chief economist with the Mortgage Bankers Association.

"There is no national housing bubble,"

"Strong economic growth means relative incomes are rising, and rising incomes help people meet their mortgage payment"

"We have pointed out that employment is key and economic performance is key and that barring any substantial changes there, we do not believe there will be significant consequences of a slowdown in the housing sector"

"tiny bubbles"Doug Duncan sounds like the perfect spokesperson for the MBA. We will be hearing much more from Doug.

But most buyers, he says, see their homes as a place to live or to retire, with appreciation as "the frosting on the cake"

Friday, August 26, 2005

Greenspan: housing boom an economic imbalance that could end badly

Greenspan's speech in Jackson Hole, Wyoming. Here are some quotes and the translation:

Thus, this vast increase in the market value of asset claims is in part the indirect result of investors accepting lower compensation for risk. Such an increase in market value is too often viewed by market participants as structural and permanent. To some extent, those higher values may be reflecting the increased flexibility and resilience of our economy. But what they perceive as newly abundant liquidity can readily disappear. Any onset of increased investor caution elevates risk premiums and, as a consequence, lowers asset values and promotes the liquidation of the debt that supported higher asset prices. This is the reason that history has not dealt kindly with the aftermath of protracted periods of low risk premiums.The foreigners and hedge funds have been buying up lots of bundled mortgages. They have accepted low compensation ( low interest rates) for their risk. This will not last. Once the incredible amount of cheap financing comes to a close the local housing bubbles will collapse. Watch out.

Don't blame me I have been flexible. We still can correct America's imbalances ( housing boom and trade deficit) without a recession.

If we can maintain an adequate degree of flexibility, some of America's economic imbalances, most notably the large current account deficit and the housing boom, can be rectified by adjustments in prices, interest rates, and exchange rates rather than through more-wrenching changes in output, incomes, and employment

Thank me. I'm Greenspan.

In fact, the performance of the U.S. economy in recent years, despite shocks that in the past would have surely produced marked economic contraction, offers the clearest evidence that we have benefited from an enhanced resilience and flexibility.

Meeting a Flipper

Last night, I was at a mid priced restaurant in the Chicago suburbs when my mom introduced me to a friend of hers. She told him about my interest in the housing bubble, and told me about his condo in the Miami area. This friend owns a successful retail store in Chicago and is also a flipper. He said that he already made one successful flip on a property. Now, he is holding another condo in a suburb of Miami and has owned it for less then a year. Part of the conversation went something like this:

Flipper "So you think that prices will decline? By how much in Miami?"

Me: "Prices will decline in Miami. By probably 20 - 30% inflation adjusted."

Flipper: "When will the start declines?"

Me: "Probably, starting the fall and continuing for a couple of years. You should consider selling now. "

Flipper: "I need to hold it until next year because of the capital gains tax issue."

Me: "Ok. They are building 60,000 condo units in Miami. Thats huge"

Flipper: "What about all the 1000 people a day who are moving to southern Florida?"

Me: "Sure. But will they be able to afford an expensive condo? Are you losing money each month on your property?"

Flipper: "Ya, I am losing a few hundred dollars a month."

Me: "If you hold you will be burned."

Flipper: "Good bye" and walks away.

Flipper "So you think that prices will decline? By how much in Miami?"

Me: "Prices will decline in Miami. By probably 20 - 30% inflation adjusted."

Flipper: "When will the start declines?"

Me: "Probably, starting the fall and continuing for a couple of years. You should consider selling now. "

Flipper: "I need to hold it until next year because of the capital gains tax issue."

Me: "Ok. They are building 60,000 condo units in Miami. Thats huge"

Flipper: "What about all the 1000 people a day who are moving to southern Florida?"

Me: "Sure. But will they be able to afford an expensive condo? Are you losing money each month on your property?"

Flipper: "Ya, I am losing a few hundred dollars a month."

Me: "If you hold you will be burned."

Flipper: "Good bye" and walks away.

Thursday, August 25, 2005

Mortgage Brokers Association Report

Today, the Mortgage Brokers Association (MBA) has released a major report regarding the housing bubble. Here is the conclusion of the report:

In this report, the MBA is downplaying the risks associated with the housing bubble. They admit there are risks and a possibility of 'localized decline' but that the would not be a 'more widespread problem.' Basically, they are saying that there maybe small price declines in certain areas or regions but that widespread price declines will not occur.

Or simply put: "Don't worry be happy" and "No need for government regulation" and "Let the good times roll"

The homeownership rate in the U.S. is now over 69 percent (chart 58). According to the American Housing Survey, of these homeowners, approximately 35 percent own their home free and clear. Another 51 percent have a fixed-rate mortgage. These 86 percent of owners benefit from house price increases and would not be affected, in terms of their mortgage payment, by an increase in interest rates.

Of the remaining homeowners, a significant number hold jumbo mortgages, indicating that they have an appreciable level of income and wealth. Another group of ARM borrowers have been in their loans for years, and their mortgage payment behavior is known. There is only a small percentage of borrowers that are potentially vulnerable to an increase in rates or other economic shock. This overall position and reassuring macro context needs to be kept in mind when determining the potential impact of the several risk factors discussed within this study. There is no suggestion that we live in a brave new world immune from risk or the possibility of a downturn.

There are a number of risk factors that should be continuously monitored. However, the appropriate stance is one of caution, not of panic. It is important that policymakers and others recognize the fundamentals that are driving the housing market. We need to understand the benefits that can be derived from innovations in the mortgage market. And, we need to identify the mitigating factors that are present in today’s mortgage and financial markets that would prevent a regional downturn or other localized decline from creating a more widespread problem.

In this report, the MBA is downplaying the risks associated with the housing bubble. They admit there are risks and a possibility of 'localized decline' but that the would not be a 'more widespread problem.' Basically, they are saying that there maybe small price declines in certain areas or regions but that widespread price declines will not occur.

Or simply put: "Don't worry be happy" and "No need for government regulation" and "Let the good times roll"

NYTimes: Rents Up

The NYTimes is reporting that 'Rents Head Up as Home Prices Put Off Buyers.' We know that in many bubble markets rents have been relatively steady or falling during the housing bubble ( ie San Francisco.) . Now as the housing bubble is reaching its peak rents are rising.

Click on image for large version

This report does not include Single Family Housing (SFH) that are available for rent. In many of the bubble markets the rent prices for SFH has been decreasing as speculators and flippers compete against each other for tenants.

Major metropolitan areas had an average rent increase of just 2.5 percent which is less then inflation and certainly less then the increase in price for a condo. Despite the recent rent increases for apartments there are still many good reasons to be a renter.

Rents in about 85 percent of large metropolitan areas have climbed in the last year, according to Global Real Analytics, a research company in San Francisco.

Nationwide, the vacancy rate for rentals fell to 9.8 percent in the second quarter after having climbed early in 2004 to 10.4 percent, the highest level since the Census Bureau began keeping statistics in 1956.

The average rent nationwide rose 2.5 percent from the spring of 2004 to this spring. It had fallen 4.5 percent from 2001 to 2003, according to Global Real Analytics.

This report does not include Single Family Housing (SFH) that are available for rent. In many of the bubble markets the rent prices for SFH has been decreasing as speculators and flippers compete against each other for tenants.

Major metropolitan areas had an average rent increase of just 2.5 percent which is less then inflation and certainly less then the increase in price for a condo. Despite the recent rent increases for apartments there are still many good reasons to be a renter.

Wednesday, August 24, 2005

Bubble Meter Blog mentioned in Washington Times

In an article titled Reflections in the Bubble in today's Washington Times it mentions this blog.

This does not exhaust the signs of a housing bubble. Those with an interest can find growing numbers of Web sites devoted to the topic. Among them are http://bubblemeter.blogspot.com, http://thehousingbubble2.blogspot.com, and http://housebubble.com.Yipee! Hooray! :-) It feels great to have this kind of publicity.

HBAS # 6: "The real reason for the housing boom is that American families are getting wealthier"

Interesting argument. This argument appeared in The Conservative Voice magazine under the title There is No Housing Bubble!! . You always need to wonder about a story title that has two exclamation points in it. Joking aside the author writes:

"The real reason for the housing boom is that American families are getting wealthier, which means they can afford to buy bigger and better housing, while the monthly cost of financing those upscale homes out of current income has dropped significantly with the lower mortgage rates"Wealth is creating this housing boom? Hmm.

- Incomes are stagnating

- Savings rates are now at zero

- The 'wealth' that is being generated is because of the housing boom.

A Proposed Exotic Loan

The lenders maybe running out of ideas to get people into homes. Here is my new exotic loan plan:

- Interest Only

- Adustable Rate Mortgage

- Negative Amortization

- No Doc ( aka 'Liar Loan' )

- 50 Year

- Bad Credit

- Bank gets 50% of future price appreciation ( not inflation adjusted)

A Realtor Bubble?

The National Association of Realtors ( NAR) just issued a study showing information about Realtors' members.

These numbers represent just NAR members.

- Members who have been in the business for two years or less earned only $12,850.Members who have been in business for 6 to 10 years earned a median $58,700 in 2004, up 18.6 percent from 2002. Members with at least 26 years of experience earned $92,600, up 37.2 percent from two years earlier.

- NAR membership totals increased 26.6 percent to 1.1 million.Between 2002 and 2004

- Sixteen percent of members own at least one vacation home. Additionally, 39 percent own additional residential properties for investment (outside of primary residences and vacation homes), and 13 percent hold an ownership interest in at least one commercial property.

These numbers represent just NAR members.

Monday, August 22, 2005

Contributing Factors

Here is my list of contributing factors that are responsible for the housing bubble. They are in order of most significant to least significant:

- Low interest rates

- Lax lending standards / exotic loans

- Greed ( flippers, speculators)

- The tech bubble ( people were less likely to invest in the stock market)

- A perceived lack of housing units to accommodate future growth

Sunday, August 21, 2005

NAR: Cautions Buyers on Specialty Loans

The National Association of Realtors warned homebuyers about 'specialty' loans or exotic loans. They warned:

Homebuyers may not realize that monthly payments on some types of specialty mortgages can increase by as much as 50 percent or more when the introductory period ends.Its about time the people in leadership are warning homebuyers about the risks of these exotic loans. It is too little too late. It is not enough to warn people about these loans. These loans should NOT be issued to many of the people they are lent to.

“The growth of the specialty mortgage market has helped many borrowers finance the American dream of homeownership, but these mortgages come with risks,” says NAR President Al Mansell of Salt Lake City. “Consumers are susceptible to loans with monthly payments that can spike dramatically, or that actually increase the amount they owe on their home. Homebuyers should consult with a REALTOR® to learn about different financing options and their implications over time.”

Because homebuyers turn first to REALTORS® for advice on the real estate transaction, NAR is making the brochure available online to all of its 1 million-plus members at REALTOR.org. Buyers can ask their REALTORS® for a copy. The brochure also is available through the Center for Responsible Lending's Web site.

Friday, August 19, 2005

Ditech.com 's Owning vs. Renting Calculator

Check out Ditech's online Owning vs Renting Calculator. Here are some problems that I found with the calculator:

- It does not count maintenance costs for a house.

- It counts appreciation of the home, but NOT investment of the monthly savings of renting vs owning. You would earn interest on this amount.

- It does NOT allow negative appreciation

Thursday, August 18, 2005

Short Term Consequences of the Housing Bubble

The housing bubble has many effects. What are the pluses and minuses of this housing bubble? Tthe below lists are just some of the effects of the housing bubble.

Short Term Minuses ( while the housing bubble has not popped )

Short Term Pluses ( while the housing bubble has not popped)

- 'Helping' the economy

- Jobs being created

- Strong consumer spending

- Rising amount of assets

- Significantly reduced amount of affordable housing

- People stretching and overextending themselves to buy houses ( 'house poor')

- Lack of investment in export orientated industries.

- Contributes to the trade deficit by encouraging more spending by people using home equity loans

Why I Blog About the Housing Bubble

Why do I devote about 8 hours a week reading and or writing about the housing bubble? There are two main reasons. The below reasons are not neccasarily in order.

- It is really fascinating

- I am being an 'economic activist' in the sense that my writings in a very very small way help influence people's actions. I am no longer just sitting on the sidelines and watching. The truth about the housing bubble needs to be revealed to a wider audience. The destructive nature of the housing bubble has gone on long enough. It is time for some economic reality. We need tradables to export to other countries.

Wednesday, August 17, 2005

Ad for Loan: HomeLoanCenter.com

Here is the home mortgage advertisement that I found off of a link from the front page on Yahoo.com

So what are some of the terms and conditions?

So what are some of the terms and conditions?

Start rate of 1.00% is fixed for the first 30 days. Fixed payment option is available for the first 12 months. Terms of the payment are based on a margin of 2.10% plus the 1 month MTA Index (2.022% as of February 16, 2005). APR of 4.27% and payment of $643.28 per month is based on a 30-year term, $200,000 loan amount at 1.00%, and may change if the index adjusts after the first 30 days. If minimum payment option is selected, deferred interest may accrue. Interest rate quoted assumes a credit score of 620+ with a loan-to-value (LTV) of 80% on a primary residence. The APR and payment will vary based on the specific terms of the loan selected and verification of information and credit. Rates are subject to change without notice.This exotic home loan the interest rates adjust after a mere 30 days. It is completely absurd. Where is the corporate responsibility? Where is the personal responsibility? If I were a potential buyer, I would refuse to even do business with a company that offers such absurd loans products. The exotic mortgage loan peddlers are being squeezed by rising short term interest rates. Many of these exotic home loan peddling companies deserve to be squeezed into oblivion.

Tuesday, August 16, 2005

Mr. Housing Bubble T-Shirts

Check out these Mr. Housing Bubble T-Shirts available from T-shirt Humor .

I may just have to get one. :-)

I may just have to get one. :-)

Monday, August 15, 2005

The Perfect Storm

A perfect storm is happening that will cause the popping of the bubble ( significant price declines in the bubble markets). What are the factors causing this perfect storm?

- New bankruptcy laws ( October 17th)

- Huge amount of consumer debt

- Minimum credit card payments may double

- Rising short term interest rates

- End of the summer buying season.

- High and rising energy prices ( ~ $65 a barrel for oil)

- Rising inventory ( part of the stagnation trend )

- Rising awareness of the housing bubble

The bubble is about to pop in the bubble cities. Stagnation will be followed by price declines. Get ready.

Sunday, August 14, 2005

Monthly Payments on Exotic Loans Rising

Interest rates on exotic loans have been rising recently as short term interest rates continue to rise. Monthly payments are thus also rising.

The above graph shows national rates for a 3 year adjustable rate / interest only mortgage loan. Exotic loans are looking less hot.

The above graph shows national rates for a 3 year adjustable rate / interest only mortgage loan. Exotic loans are looking less hot.

The above graph shows national rates for a 3 year adjustable rate / interest only mortgage loan. Exotic loans are looking less hot.

The above graph shows national rates for a 3 year adjustable rate / interest only mortgage loan. Exotic loans are looking less hot.

Interview w/ David Lereah & Bubble Meter

Smart Money magazine recently had an interview with David Lereah who is the chief economist for the National Association of Realtors. Bubble Meter was not actually interviewed. Here are the questions and answers:

Smart Money: This week you said that we might be near a peak in the real-estate market. Should people be worried about the price of their homes?

Lereah: "'I've been saying that for two, three years now: That we're finally at a peak for home sales. And we continue to be wrong. We do think right now we may be at a peak, and that home sales should come down a bit as mortgage rates continue to rise."

Bubble Meter: "You did not properly answer the question. The question was about the price of a home, and not about the number of home sales. Or maybe you meant home prices when you said home sale. Either way you need to be clearer. That being said I think those who live in the bubble markets and can comfortably make the payments and have a desire to live in their house for the long run do not need to worry about price declines. People who are overextended on their (owner occupied) home mortgage need to be concerned. Those who are investors, speculators and are renting out their property at a loss so they can gain price appreciation need to worry. There will be price declines in the bubble locales."

"Do you think the real-estate market will still be able to provide a sound investment?"

Lereah: "Real estate is still a great investment opportunity for households. Price appreciation will continue. It may not be at 20%. It may be at 10% to 15%, or may even go down to 5%. The returns are still going to be good, but not as great as they have been. Real estate should still be extremely competitive [in terms of] return on investment. You don't need a 20% price appreciation to do well. You could still have price appreciation of 10% and beat most stocks. I think for the remaining years of this decade real estate will still be a good investment.

I think real estate is still a very attractive investment — to buy or to live in. I think price appreciation will continue. I don't think there will be a price-appreciation pop. It's not going to be nationwide. The fundamentals are there. The demography trends and population trends are there. It's a once-in-a-generation opportunity.

Bubble Meter: "There will be opportunities in certain locations. But, in the bubble markets the peak has either been reached or is coming shortly. I would not invest in the bubble markets right now. The bubble markets include Miami, LA, San Diego, San Francisco, Bakersfield, Seattle, Phoenix, NYC, Boston and many others locales.”

Smart Money: I'm assuming you don't believe in the existence of a housing bubble.

Lereah: No, I don't think there is one. You may see some air come out of some of those balloons. It might go from 20% appreciation to 5%. Housing [price appreciation], historically, is between 3% and 6% [annually] — somewhere in that range. So if you can do better than 6%, you're doing great. Even 5% is still very good.

BubbleMeter: "Yes there is definitely a housing bubble in the bubble markets. The bubble markets include many of the major cities. You can expect price declines in these markets. "

Smart Money: What if people interested in investing in real estate come to expect 20%-plus price appreciation on their homes, and won't be willing to settle for just 5%?

Lereah: I think that we'll probably knock out a certain percentage of investors. But the ones who remain will do very well. Remember, a 5% price appreciation gives you a lot bigger return than 5% because you're buying real estate on margin. You're giving a down payment. Say you put down $10,000 on a $100,000 house. If it increases by 10%, you get $10,000. That's a 100% return.

Bubble Meter: "Mr. Lereah is totally ignoring the carrying costs. On recent investor purchases, in the bubble markets the rent is not covering the mortgage, taxes and maintenance costs. Thus each month, you are losing money on your investment. Will you be able to make it based upon future price appreciation? Nope. Price declines are expected in the bubble markets."

Smart Money: If a peak, in your opinion, is close at hand, should investors stay away from real estate?

Lereah: There's still momentum. It's still a very healthy market with a lot of demand. It looks like if interest rates continue to go up maybe we've hit a peak in terms of home sales. We do expect the Fed to continue to raise rates a quarter percent each time. Each time they do that, mortgage rates will get a little bit higher. But again we're still going to be at healthy levels.

Friday, August 12, 2005

The Bubble Recession

Once the housing bubble pops, a recession is almost inevitable. Here are the factors that will contribute to a future recession:

- High & Rising Energy Costs

- Federal Debt & Deficit

- Coming Housing Bust

- High Consumer Debt

- Large negative Trade Balance

- Future Offshoring

- Security Costs

So are there bright spots? Corporate profits are doing well, productivity is up. Nevertheless, the overwhelming negative economic factors will shortly ( within a year or so ) lead us into a recession. The unsustainable nature of our economy is astounding.

Thursday, August 11, 2005

Bubble Watching

The housing bubble has certianly affected many locales. But there are certain places that I'll be particulary watching for stagnation and price declines. Here is my list of bubble places I'll be closely watching:

- San Diego

- Las Vegas

- Bakersfield

- Miami

- Boston

- Washington, DC ( huge price appreciation, strong fed related job growth)

Wednesday, August 10, 2005

Bubble Places: Pahrump, Nevada

Ever heard of Pahrump, NV? I thought not. Well, if you are Las Vages real estate person or housing bubble follower you might have.

What is the significance of Pahrump, Nevada in relationship to the housing bubble?

It is a place literally located in a largely undeveloped desert valley that is being turned into a bedroom community of Las Vegas. Housing prices have skyrocketed. It is a fascinating place to follow the housing bubble.

Where is Pahrump, Nevada?

Pahrump, NV is located about 64 miles west of Las Vegas. It is in a large desert valley. Check out the Google Map image of Pahrump.

Highway 160 running Through Pahrump

Calvada Eye

Downtown Pahrump

Junk in Pahrump

What is the significance of Pahrump, Nevada in relationship to the housing bubble?

It is a place literally located in a largely undeveloped desert valley that is being turned into a bedroom community of Las Vegas. Housing prices have skyrocketed. It is a fascinating place to follow the housing bubble.

Where is Pahrump, Nevada?

Pahrump, NV is located about 64 miles west of Las Vegas. It is in a large desert valley. Check out the Google Map image of Pahrump.

Can I see some pictures?

What is happening in the local real estate market?

Check out this Pahrump Real Estate site .

There will be more bubble places featured in the future. Stay tuned.

Tuesday, August 09, 2005

Debunking Greenspan

Once again, Greenspan increased short term interest rates by 25 basis point ( or .25). The short term interest rates now stand at 3.5% . Greenspan's move was expected. No surprises here. Here are some highlights from the Federal Reserve Board Press Release:

Greenspan is pathetic. He should resign sooner, rather then later. The credit bubble has been 'great' for the short term ( 2001 - 2005 ), but it will be disastrous for the long term. Neglect the long term for the short term, that is Greenspan's gameplan. Remember, "With great power comes great responsibility."

This should be written to "Aggregate spending, despite high energy prices and because of the credit bubble [ which this Federal Reserve Board is partially to blame ], appears to have strengthened since late winter. The labor market conditions continue to improve gradually based on an unsustainable housing bubble and reckless consumer spending ""Aggregate spending, despite high energy prices, appears to have strengthened since late winter, and labor market conditions continue to improve gradually"

"Core inflation has been relatively low in recent months and longer-term inflation expectations remain well contained, but pressures on inflation have stayed elevated."How about housing prices and energy costs? Oh, I forgot they are not included in the CPI.

How about doing more to maintain lending standards? Wait, every American has the right to get a 500K loan even though they have a 70K income, zero money for a down payment and credit score of 600."Nonetheless, the Committee will respond to changes in economic prospects as needed to fulfill its obligation to maintain price stability"

Greenspan is pathetic. He should resign sooner, rather then later. The credit bubble has been 'great' for the short term ( 2001 - 2005 ), but it will be disastrous for the long term. Neglect the long term for the short term, that is Greenspan's gameplan. Remember, "With great power comes great responsibility."

HBAS #4: "Everyone Needs a place to Live'

The housing bubble argument that says 'Everyone needs a place to live' is probably the most ridiculous one out there. The implication is that therefore prices will continue to rise or that prices won't decline. Here is my response:

- People do not need to buy. People can and do rent.

- People do not have to live in a bubble market. They may move to cheaper locales.

- There is a practical limit on what people can afford based on income, other expenses, interest rates, and lending standards

- Many of the people now buying are not living there, they are renting ( or trying to rent) their highly leveraged housing units.

- People have always needed 'a place to live,' which did not stop prices from falling in California in the early 90's

Another Housing Bull Argument ( HBA ) debunked.

Monday, August 08, 2005

Krugman: That Hissing Sound

Paul Krugman in today's NYTimes writes "This is the way the bubble ends: not with a pop, but with a hiss. Housing prices move much more slowly than stock prices. " This is certainly true. However, let us compare it to other housing bubbles. For a housing bubble, this has been an incredible speculative episode, and thus compared to other periods of housing price appreciation there is going to be a larger drop in prices. Perhaps a 'loud hiss' would be an appropriate term.

Sunday, August 07, 2005

Realtor.com Traffic Peak?

Web traffic on the Realtor.com website may have peaked. "The June traffic also is a 28 percent increase over June 2004," however the site "received 7.28 million unique visitors in May and 7.27 million unique visitors in June." Therefore, traffic is actually down ever so slightly from May. Was this the peak? Does this foreshadow the end of the housing boom? The anecdotal evidence is building.

Friday, August 05, 2005

TOLL Brothers' Stock Down

The Toll Brothers' stock tanked today, falling 7%, which is quite significant.

Toll Brothers has made a fortune off of the housing bubble. The peak has been reached.

Toll Brothers has made a fortune off of the housing bubble. The peak has been reached.

David Lereah on the Housing Market

David Lereah who is the chief economist for the National Association of Realtors (NAR) writes this in a recent NAR news release:

This is changing as we speak. Inventory is growing in much of the country. By the end of the year price declines will be occuring in many of the bubble markets.

He is saying that there will be 'soft landing' in the bubble markets. This is a far cry from the position he took just a few months ago when he denied the existence of a bubble.

Maybe, but that will be soley based on the first half of the year. Th last four months of the year the housing market will be either stagnating or declining. The bubble is about to burst. The continued price appreciation is unsustainable. Widespread price declines in the bubble markets are around the corner.

“The simple fact is we still have more buyers than sellers in most of the country,” says Lereah. “This supply-demand imbalance is continuing to put pressure on home prices, but we should get closer to equilibrium by the end of the year.”

This is changing as we speak. Inventory is growing in much of the country. By the end of the year price declines will be occuring in many of the bubble markets.

The home price-to-income ratio is alarmingly high, especially in California, rising from 23 percent in 2003 to 32 percent in 2004,”

In the past year, ARMs have made up 30 to 40 percent of mortgage loans, when they should actually be around 25 percent. “The increase in the use of adjustable rate mortgages at a time when fixed mortgage rates are at historic lows is troubling.”It is indeed very troubling.

''Obviously, there are some local bubbles,'' Lereah says. ''But I tend to think that with most of the bubbles, the air will come out slowly, rather than popping.''

He is saying that there will be 'soft landing' in the bubble markets. This is a far cry from the position he took just a few months ago when he denied the existence of a bubble.

Relative to inflation, home prices will continue to experience above-average returns in 2005

Maybe, but that will be soley based on the first half of the year. Th last four months of the year the housing market will be either stagnating or declining. The bubble is about to burst. The continued price appreciation is unsustainable. Widespread price declines in the bubble markets are around the corner.

Thursday, August 04, 2005

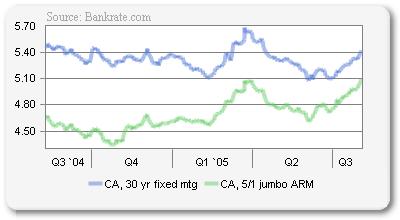

Jumbo 5/1 ARM vs. 30 Year Fixed

Here is a graph from Bankrate.com showing the interest rates on a 5/1 ARM Jumbo Loan vs. a 30 year fixed loan (for loans originating in California):

Notice how the difference in interest rates is narrowing. Hopefully, the allure of these Adjustable Rate mortgage Loans will wane.

Notice how the difference in interest rates is narrowing. Hopefully, the allure of these Adjustable Rate mortgage Loans will wane.

HBAS #3: Explaining why the Price "bubble is being sustained'

Here is a housinghead argument taken from the Housing Bubble Blog. Read it carefully: (HBAS = Housing Bull Arguments Series)

The explosion of housing bubble news has changed the demand curve in the bubble markets. People are less eager to buy. Since, home affordability is at such lows in the bubble markets, the renters for the large part have given up on homeownership until prices declines occur or until their incomes go up ( in the bubble markets). But, with incomes stagnating, income gains will not be sufficient to continue the bubble.

In case anyone was wondering how the price bubble is being sustained. It's being sustained by the 30%renters waiting and waiting and waiting and finally buying in 06, 07, 08, 09, 2010 as the 'bubble' continues and price increases through the end of the decade. "This housing bull has an interesting argument. In fact the person admits that there is a 'price bubble', but that there will be "price increases through the end of the decade." It is not about if there is a bubble or not, the argument of this poster is merely about timing. The poster states that the price increases are "being sustained by the 30% renters waiting and waiting and waiting and finally buying in 06, 07, 08, 09, 2010." First of all homeownership is at an all time high of 69%. Many, of the people in last remaining percentage of people are either too poor, not interested, or too mobile to own a home.

The explosion of housing bubble news has changed the demand curve in the bubble markets. People are less eager to buy. Since, home affordability is at such lows in the bubble markets, the renters for the large part have given up on homeownership until prices declines occur or until their incomes go up ( in the bubble markets). But, with incomes stagnating, income gains will not be sufficient to continue the bubble.

Wednesday, August 03, 2005

Overheard Conversation

I was standing in line a few days ago waiting for my food to be prepared at a local restaurant in Silver Spring, MD (suburban Washington, DC) , when I overheard a real estate related conversation. It went something like this:

Patron: "So how's life? "

Restaurant Server: "Good thanks. [Pause] "How is your new business?"

Patron: "Slowing down. As the prices are very expensive and mortgages rates are rising."

Restaurant Server "Keep plugging. Things are slowing down in general."

Patron "Thanks. [ picking up the food] Have a great day."

Keep you ears and eyes open. This blog adores personal housing bubble related stories submitted by users. :-) Please post them.

Patron: "So how's life? "

Restaurant Server: "Good thanks. [Pause] "How is your new business?"

Patron: "Slowing down. As the prices are very expensive and mortgages rates are rising."

Restaurant Server "Keep plugging. Things are slowing down in general."

Patron "Thanks. [ picking up the food] Have a great day."

Keep you ears and eyes open. This blog adores personal housing bubble related stories submitted by users. :-) Please post them.

Reader's Suggested Topics

It would be great to hear from readers what topics they would like to discuss. Please post in the comments section for this post what topics interest you (within the housing bubble realm). Thanks.

Tuesday, August 02, 2005

HBAS #2: 'They are Not Making Anymore Land"

One often heard housing bull argument (HBA) is that 'they are not making anymore land' and thus housing unit prices will go up because supply is constrained. While it is basically true that they are not making anymore land, land is not the same as a housing unit. Consider these points:

- They may not be creating anymore horizontal land, but 'vertical land' is being created at a furious pace. Condos are vertical land.

- In many of the bubble cities there is plenty of land to sprawl onto (think Sacramento, Phoenix, Boston etc.)

- Land is being made available through various sources such as the BLM ( Bureau of Land Management) and base closings.

- Certainly, they were not making anymore land during the early 1990's housing crash.

The Housing Bull Arguments Series will continue. If you have any suggested topics for upcoming posts in the HBAS please post in the comments.

Monday, August 01, 2005

Home Construction Boom & Oversupply

There is a "is a construction boom that is starting to outpace demand. America creates only about 1.2 million additional families or individuals who need new housing each year. About 400,000 houses have to be replaced because of obsolescence each year. Add in, say, 300,000 more for second or vacation homes, and the total annual demand for additional housing tops out at about 1.9 million. But builders and manufacturers are on track to create at least 2.2 million new housing units this year" ( US News & World Report, 6/6/05 ) .

The supply of housing has been outpacing the demand for housing. So who has been buying the rest? Speculators and flippers. But demand is not keeping up with supply. Perhaps, that is why for the second month in a row there has been a decline in the median price for new homes.

Housing Bull Arguments Series

The housing bulls have many arguments for their position. This blog will be featuring a series called 'Housing Bull Arguments' which will examine their arguments on an argument by argument basis. Today's housing bull argument is from a Slate.com Article :

The builders (suppliers) are flooding the market with new housing units. For example, look at Miami where "In Miami, the construction crane could become the new state bird as some 25,00 new units are punching into the skyline - with another 40,000 on the drawing board. (Christian Science Monitor, July 8, 2005)". Not satisfied? In California, "Home builders beat a record established in 1989 by starting construction on more than 16,000 homes in June, the California Building Industry Association announced Thursday (EastBay Biz Journal, July 25, 2005).

The home construction industry is building, and building fast. There is no housing unit supply shortage. Furthermore, if there was a shortage of housing units in the bubble markets the rental prices would be exploding in the bubble cities. This is not the case. Generally, rents in the bubble cities have barely kept up with inflation. There is no housing unit supply problem. Demand is the issue, as the demand curve has shifted to ridiculous levels due to the 'speculative fervor.'

Housing prices have to make sense on both the demand side and the supply side. No matter what you do or don't believe about the ability of crazed demanders to bid up prices, you still have to explain why competitive suppliers don't bid those prices right back down. In other words, if the housing market is so tight that builders are making a fortune, they ought to be flooding the market with new houses—and driving down prices

The builders (suppliers) are flooding the market with new housing units. For example, look at Miami where "In Miami, the construction crane could become the new state bird as some 25,00 new units are punching into the skyline - with another 40,000 on the drawing board. (Christian Science Monitor, July 8, 2005)". Not satisfied? In California, "Home builders beat a record established in 1989 by starting construction on more than 16,000 homes in June, the California Building Industry Association announced Thursday (EastBay Biz Journal, July 25, 2005).

For the past three years 1/3rd of the new units added are lying vacant and in the past six months 2/3rd of the new units added are lying vacant. At some point the reality of the Supply and the Demand for housing (as in living in a house and not speculating) will assert itself and all the speculative buyers will have

hell to pay." ( Financial Sense 7/31/2005 )

The home construction industry is building, and building fast. There is no housing unit supply shortage. Furthermore, if there was a shortage of housing units in the bubble markets the rental prices would be exploding in the bubble cities. This is not the case. Generally, rents in the bubble cities have barely kept up with inflation. There is no housing unit supply problem. Demand is the issue, as the demand curve has shifted to ridiculous levels due to the 'speculative fervor.'

Subscribe to:

Posts (Atom)