“The boom is cooling now,” said David Lereah, the chief economist for the association, who added that falling home sales have been “a bit worse than we had anticipated.”As chief economist of the National Association of Realtors (NAR), David Lereah, is responsible for the economic forecasts. Back on October 28th, 2005 the NAR forecasted that:

The group said that it now expected sales to fall further than it has said in the past — about 7.5 percent this year compared with an earlier projection of a 5 percent decline.

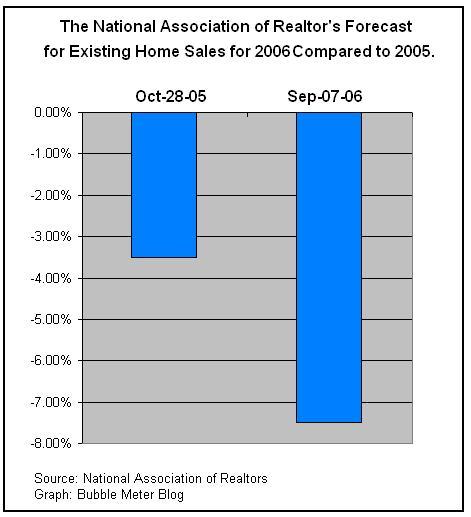

So on October 28th, 2005 the David Lereah and the NAR forecasted that there would be a decline of 3.5% in existing home sales for 2006 compared to 2005. Now, Mr. Lereah is forecasting a decline of 7.5% for 2006.Existing-home sales are projected to decline 3.5 percent in 2006 to 6.86 million. New-home sales, seen to grow by 8.0 percent to 1.30 million in 2005, are expected to fall 4.5 percent to 1.24 million next year. The figures for 2006 would be the second highest year for each sector.

The September 2006 forecast is more then double the decline of the October 2005 forecast. Despite the large adjustment from his October 2005 forecast, David Lereah says that the decline is "a bit worse than we had anticipated." This is deceptive. Due to his cheerleading and continuing deceptions Mr. Lereah cannot be trusted.

The Incredible Shrinking NAR Forecast:

ReplyDeleteJuly 11th, 2006

Existing-home sales are expected to decline 6.7 percent to 6.60 million in 2006 from 7.08 million last year. That would still be the third highest level on record. New-home sales should fall 12.8 percent this year to 1.12 million from 1.28 million in 2005. Housing starts are forecast to decline 6.8 percent to 1.93 million this year from 2.07 million in 2005.

The 30-year fixed-rate mortgage is likely to reach 7.0 percent by the end of the year. June 6th, 2006Existing-home sales are projected to drop 6.8 percent to 6.60 million this year from the record 7.08 million in 2005. New-home sales are forecast to fall 13.4 percent to 1.11 million from a record 1.28 million in 2005. Housing starts are likely to decline 6.2 percent to 1.94 million in 2006 compared with 2.07 million last year.

May 9th,2006

Existing-home sales are likely to fall 6.4 percent to 6.62 million in 2006 from a record 7.08 million last year. New-home sales are projected to drop 11.6 percent to 1.13 million from last year’s record of 1.28 million. Housing starts should decline 3.7 percent to 1.99 million this year compared with 2.07 million in 2005.

April 11th, 2006

Existing-home sales are projected to drop 6.0 percent to 6.65 million this year from a record 7.08 million in 2005. New-home sales are likely fall 10.9 percent to 1.14 million from the record 1.28 million last year – both sectors would see the third best year following 2005 and 2004. Housing starts are forecast at 2.00 million in 2006, which is 3.2 percent below the 2.07 million in total starts last year.

March 13, 2006

Existing-home sales are expected to fall 5.7 percent to 6.67 million in 2006 from

the record 7.08 million last year. At the same time, new-home sales are forecast to decline 7.7 percent to 1.18 million from a record 1.28 million in 2005 – each sector would be at the third highest year following the tallies for 2005 and 2004. Housing starts are likely to total 1.98 million this year, down 4.3 percent from 2.06 million in 2005.

February 7th, 2006

Existing-home sales are likely to decline 4.7 percent to 6.74 million this year, down from a record 7.07 million units in 2005, while new-home sales are expected to fall 8.5 percent to 1.17 million from a record 1.28 million in 2005; both sectors

would see their third best year after the totals for 2005 and 2004. Housing starts are seen at 1.87 million units in 2006, down 9.3 percent from 2.06 million last year.

The 30-year fixed-rate mortgage should rise to 6.9 percent by the end of the year.January 10th, 2006

After setting a fifth consecutive annual record, projected to 7.10 million units for 2005, * existing-home sales are forecast to ease by 4.4 percent to 6.79 million this year, which would be the second highest on record. New-home sales, which should be a record 1.29 million for 2005, are expected to decline 6.0 percent to 1.21 million in 2006 – that also would be the second best year in history. Total housing starts for 2005 are seen at 2.07 million units – the highest since setting a record 1972 – with a 6.6 percent slowing to 1.94 million this year. December 12th, 2005Existing-home sales, expected to rise 4.7 percent to 7.10 million this year, are likely to decline 3.7 percent in 2006 to 6.84 million. New-home sales, projected to increase 7.0 percent to 1.29 million this year, are forecast to drop 4.8 percent to 1.23 million in 2006 – also the second best on record. Total housing starts for 2005 should grow 5.8 percent to 2.06 million units, the highest since 1972, and then decline 4.8 percent to 1.92 million next year.

October 28th, 2005

Existing-home sales, which should increase 4.8 percent to 7.11 million this

year, are projected to decline 3.5 percent in 2006 to 6.86 million. New-home sales, seen to grow by 8.0 percent to 1.30 million in 2005, are expected to fall 4.5 percent to 1.24 million next year. The figures for 2006 would be the second highest year for each sector.

Total housing starts this year are forecast to be the highest since 1972, rising 5.7 percent to 2.06 million units, before declining 4.6 percent to 1.97 million in 2006.

The 30-year fixed-rate mortgage is projected to rise slowly to 6.7 percent by the end of next year.

condomania wrote "I'm sorry, but economists revise forecasts all the time."

ReplyDeleteTrue. The problem is his later statement that the decline is "a bit worse than we had anticipated." That is the DECEPTION!

"David, I would disagree. Was it deception for him to revise the forecast upward for 2004 and 2005? Economists are like weathermen, except they tell you yesterday's weather. "

ReplyDeleteNo. The problem is when Lereah later says that the revision was a 'bit worse' then anticipated when in fact the decline was over more then double what he anticipated in October.

This is deceptive. Due to his cheerleading and continuing deceptions Mr. Lereah cannot be trusted

ReplyDeleteI'll bring the tar. You bring the feathers.

I think the problem is that the NAR employs college interns who recently took their first Microsoft Excel course to provide this "comprehensive in-depth analysis".

ReplyDeleteThat, or they just make things up on the fly.

Either way, it's complete BS.

BREAKING NEWS - Median home prices in NOVA are down 8%, yes 8%, on a year over year basis for August.

ReplyDeleteSee MRIS.com for details!!!

This is way worse than even I, a super duper bubblehead, expected to happen so quickly.

va-

ReplyDeleteSpin spin. Sorry. Down is down.

OFFICIALLY DOWN 8% YOY!!!

crispy&cole

Down 8% YOY! I guess RE does go down!

ReplyDeleteExtremely interesting FACTS from the Federal Reserve.

ReplyDeleteNote that it is RENTERS who have by far the higher debt burden in the U.S.

www.federalreserve.gov/Releases/housedebt/www.federalreserve.gov/Releases/housedebt/

note, that should have been:

ReplyDeletewww.federalreserve.gov/Releases/housedebt

This comment has been removed by a blog administrator.

ReplyDeleteCondomania said...

ReplyDelete"I'm sorry, but economists revise forecasts all the time."

Lereah is not an economists.

Not to sound elitist...

ReplyDelete_________________________

Nevermind.

Mighty brazen comments. I guess David has turned comment moderation off.

ReplyDeleteva_investor said...

ReplyDelete“For God's sake. His education is in Economics. Anyone with half-a-brain knows he is a paid mouthpiece. I am sure that he is not the only economist who got it wrong.”

So, which is it? Paid mouthpiece or economist?

Lance said...

ReplyDelete“Extremely interesting FACTS from the Federal Reserve.

Note that it is RENTERS who have by far the higher debt burden in the U.S.”

Yaawwn, strrrrreeeeetch. Hummm . What’s on the hot sheets as we hit the weekend? Let’s see, Inventory up, foreclosures up, delinquency up; still have a few trillion dollars worth of ARM resets.

Oh yea, DC down 8.7% YOY. Locally, down over 8% YOY.

Have a great weekend folks, think I’ll do some fishin.

Robert said:

ReplyDelete"Oh yea, DC down 8.7% YOY. Locally, down over 8% YOY."

So you're able to buy now? Why didn't you just buy then in 2004 before it went up 22% between 2004 and 2005? Wouldn't that have been a lot cheaper than the 8% down?

2006 prices, 2005 prices

ReplyDeleteArlington County Median Sold Price: $ 420,000 $ 490,000 - 14.29 %

Alexandria Median Sold Price: $ 440,000 $ 449,000 - 2.00 %

Fairfax Median Sold Price: $ 469,000 $ 500,000 - 6.20 %

Loudoun Median Sold Price: $ 486,500 $ 506,100 - 3.87 %

Prince William Median Sold Price: $ 375,000 $ 395,000 - 5.06 %

Please no spin on these numbers. 14% is UGLY!

ReplyDeleteDavid, median DC proper prices down over 8%!

ReplyDeleteLance said...

ReplyDelete“So you're able to buy now?”

I was able to buy a year ago. I was able to buy 6 months ago. I am able to buy now.

Now go spruce up that basement apartment for your future bitter renter. Gotta get that thing rented out man! Your equity is on the line here! Hey, since DC dropped 8.7% are you gonna have to jack up the rent?

warmblanket,

ReplyDeleteInteresting post on the events leading to the Great Depression. As the great fear at the moment is that we are starting to see rampant inflation, how do you see a sudden shift to the deflation discussed in the article occuring here and now under foreseeable conditions?

OFFICIALLY DOWN 8% YOY!!!

ReplyDeletewow. That was quick.

To think, as you predicted well before I, that this really doesn't get started until 2Q2007. I did think DC was further behind Florida and California, not trying to pull up to Boston. Seriously, this is going to be a national event.

By va_investor:

If we see deflation it could portend a depression.

Hey, I get to play the optimist now! I think we'll see deflation by the 1970's definition of inflation. But right now, we focus on the "core." The core is 40% commercial rents, and those look to be flat to up for a bit. Not a lot up...

But also look at the spike in import prices. :( The "free lunch" is over. We'll have some inflation. for me, all that matters is do my assets do better than housing, for I will buy in a few years. :)

Also va_investor: Not to sound elitist, but renters have always comprised the lower class and the lower-middle class.

And quite a few others. But do recall, its a bufucated market. You have a huge number of six figure couples who feel "priced out" or cannot see the economic sanity of buying. I'm not the only one at work who has done the calculation:

In a sane housing market, one can expect to come out ahead *buying* over renting about the original purchase price of the home in 30 years.

In today's market, my most optimistic calculation shows the renter coming out ahead at least half the home's value after 30 years. :( Thus, the bubble.

Many of the other renters are students, just out of college, or the 26% of the population too close to the poverty line to qualify for credit (like a mortgage).

Lance said: So you're able to buy now? Why didn't you just buy then in 2004 before it went up 22% between 2004 and 2005? Wouldn't that have been a lot cheaper than the 8% down?

And it will be a lot cheaper in a year. The only question is how many years of equity gains are about to be given up.

So much for your previous comments about there never being a bad time to buy real estate. Recommending to buy a home now is like Cramer when he recommended tech stocks at the Nasdaq going down through 4000... Look at the funamentals. Nondimensionalize any housing variable versus historical standards and its far too obvious how out of whack the market is.

Neil