The NVAR (Northern Virginia Association of Realtors)

just posted their market summary numbers for the month of February:

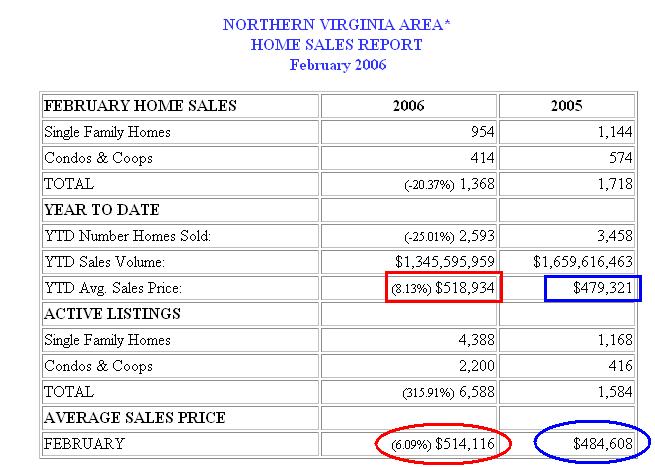

Although the volume of single family homes and condos sold in February 2006 in Northern Virginia was 20 percent below the units sold totals for February 2005, average sales prices have increased 6 percent, to $514,116. More than four times as many active listings were on the Northern Virginia market in February 2006 than February 2005, up 316 percent from 1,584 to 6,588.

February 2006 sales volume in the Greater Northern Virginia region was also more than 20 percent below volume in February 2005. Sales prices, however, have increased 9 percent, to $483,872. Greater Northern Virginia includes Fairfax County, Fairfax City, Arlington County, Alexandria, Falls Church, as well as Prince William, Loudoun, Fauquier, Culpeper, Madison, Clark, and Rappahannock counties.

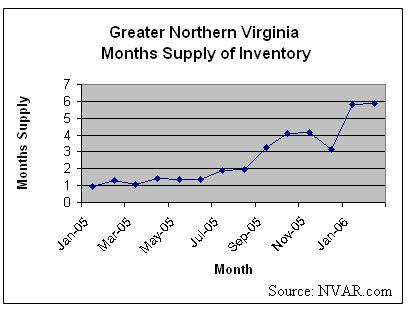

Active listings in the Greater Northern Virginia area were significantly higher in February this year than in 2005. February's total of 14,662 active listings were more than 250 percent greater than the number last year, which was 4,173.

But here is where it gets interesting:

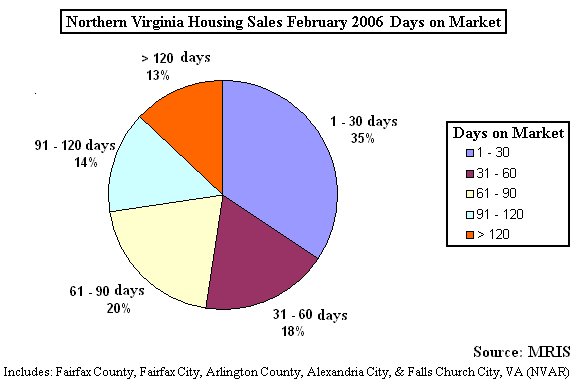

These numbers here are for single family homes, condos & coops sold in Northern Virginia. Which include "C

ounties of F

airfax and Arlington, and the cities of Alexandria, Falls Church, Fairfax, and the towns of Vienna, Herndon and Clifton"

Please note that the 2005 YTD (year to date) Avg Sales Price number (blue square) which is 479,321 does not match the number listed in the February 2005 Northern Virginia Report which is 479,935. When you do the math for the numbers, the 2005 reports makes sense as $1,659,616,463 divided by 3,458 equals 479,935 and not 479,321.

There is an error here in the NVAR data. The difference between the numbers is only $614.

In Northern Virginia, for

January 2006 the YoY (year over year) average percentage price increase was 10.03%

which is more then the February 2006 YoY average price increase of 6.09% (red circle). As we move further into the year, the year over year percentage increase continues to fall. The same pattern has happened for the Greater Northern Virginia area.

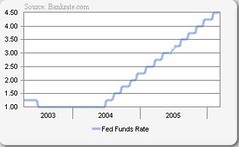

By April 2006, the YoY sales price increase will be NEGATIVE for Northern Virginia. There will be no spring boom this year.