The total number of housing units sold in May 2006 declined 32% compared to May 2005. Northern Virginia includes "Fairfax County, Fairfax City, Arlington County, Alexandria City, & Falls Church City, VA"

The total number of housing units sold in May 2006 declined 32% compared to May 2005. Northern Virginia includes "Fairfax County, Fairfax City, Arlington County, Alexandria City, & Falls Church City, VA"The number of active listings in Northern Virginia stood at 11554 in May 2006, which represents an increase of 240.3% from May 2005 when active listings were at 3395. The average days on market (DOM) for housing units that sold in May 2006 was 51 which was 240% more days then the 15 days in recorded in May 2005.

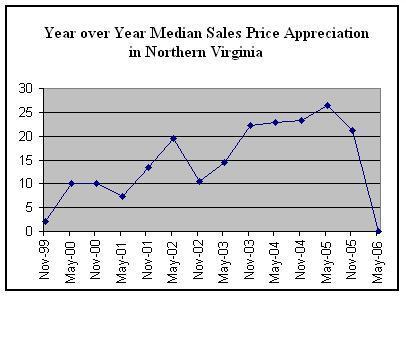

In Northern Virginia there is a declining number of sales, declining real dollar prices, and an exploding amount of housing inventory. There will be no soft landing in Northern Virginia or in other bubble markets.

Can you show the chart for Metro DC?

ReplyDeleteits not available for the whole DC region. The charts are available by county.

ReplyDeletedavid, could you please show the DC chart? thx

ReplyDeleteFortunately that curves is going to take a very hard turn and will transition into the soft landing scenario. No YoY declines because that would be unthinkable.

ReplyDeletelance,

ReplyDeletelater this week in a seperate posting. I need to make a DC Chart

LOL. Some of the bubble deniers on here claim David only hates DC the city. Then when he covers the suburbs, other deniers show up and ask for DC city data.

ReplyDeleteIt is important to realize that real prices are down. This means that the people who bought last year at the height of the hysteria are S.O.L. and have lost money on their investment. That will act as a discouragement for further "investment."

A Redskins fan

Okay, I went and examined the DC proper numbers at MRIS.

ReplyDeleteYOY Median price down 1.18%. With inflation, that's a decent-size real decline.

Median Sold Price:

$420,000 $425,000 - 1.18 %

But average price is up 6.26%. Even though the average price is the worse statistical measure, I thought I'd mention it just to throw Lance a bone.

David, why would you adjust for inflation if you're insisting that there's deflation in the housing market? Most people who sell their home buy another home.

ReplyDelete"Even though the average price is the worse statistical measure" because it doesn't support the bubbleheads' preferred conclusion ...

ReplyDeleteSo home prices are up more than 100% in the last six years. And now, for the sake of discussion, we are in for three years of 10% price delcines? So they're still up over 70%.

ReplyDeleteNot a problem for most homeowners. It is stressful for people who bought last year, but otherwise, what's the big deal?

"David, why would you adjust for inflation if you're insisting that there's deflation in the housing market? Most people who sell their home buy another home. "

ReplyDeleteIf you are a flipper or specuvestor it is a real problem. Also the 'loss' of wealth is a drag effect on the economy in the short term

great article taking on the NAR....from a very reputable source

ReplyDeletehttp://www.fool.com/news/commentary/2006/commentary06060918.htm

anon 6:04

ReplyDeletethanks. I made a new post.

Hey Anon 5:18...

ReplyDeleteYou need to revisit your own calculations. You said: "So home prices are up more than 100% in the last six years. And now, for the sake of discussion, we are in for three years of 10% price delcines? So they're still up over 70%"

My response: Assume a house that sells six years ago for $200K has appreciated by 100%. That house is now worth $400K. Then...assuming over the next 3 years declines of 10% per year, after year 1, it will be worth $360K; year 2, $324K; Year 3, $292K. Yes, they are still up, but by much less than the off the cuff 70% you state. Extend those 10% losses 2 more years to 5, and the price is now $235K.

Also note: the above is NOMINAL and not adjusted for inflation.

Your post highlights the dangers inherent in a math-challenged public of borrowers getting in over their heads without even knowing it's happening.

"If you are a flipper or specuvestor it is a real problem. Also the 'loss' of wealth is a drag effect on the economy in the short term "

ReplyDeleteSo, basically you're doing it for no reason other than that it supports your preferred conclusion. thanks for clearing that up.

"why would you adjust for inflation if you're insisting that there's deflation in the housing market? Most people who sell their home buy another home."

ReplyDeleteUmmm.... I don't know if that is true for what happened in 2003-2005. A lot of people were buying multiple homes with the intention of using them as "investment" properties. I don't know if it was "most" or not, but it was a lot. The point is, if there are much better real investments out there (and over the last year, it seems to me there were), then why make huge leveraged bets on real estate?

Also, even if you are buying only to live in the house, it still might be better to wait a few years, rent, and make more money on other investments so that when you do buy, you get a better financial situation for yourself.

So the real return is very relevant.

A Redskins fan

Dear David,

ReplyDeletePlease reconcile these facts to your outlook:

http://sungazette.net/articles/2006/06/12/arlington/news/nws933.txt

Thank you.

Anonymous, the article uses the MRIS numbers for Arlington County. The article mentions the average price gain on 9%, but doesn't mention the median price change of 2%, which is basically 0 in real dollars. So it's a very cheerleady article.

ReplyDeleteHere's a basic lesson is statistics, since I was falsley accused of cherrypicking some data points earlier by some ignorant anonymous poster:

When you have skewed data, medians are more informative than averages.

By skewed, I refer to cases where there a few very large observations could drive the averages. Changes in Bill Gates or Donald Trump's incomes may change average incomes a lot, but won't tell us what's going on with most people. You'd look at medians for that.

By the same token, a sale of one $5 mill house will drive the average homes sales price by quite a bit, but won't tell you what's going on with the housing market as a whole. You'd use medians for that, too.

Hopes this helps those who are actually interested in learning and understanding.

"Dear David,

ReplyDeletePlease reconcile these facts to your outlook:

http://sungazette.net/articles/2006/06/12/arlington/news/nws933.txt

Thank you."

Please point out specific examples (quote me and the article) where the facts do NOT reconcile. I saw nowhere in the article where the facts are specilfically opposing to anything in my post.

Thanks

thanks keith for a solid explanation!

ReplyDeleteKeith, you have no reason to believe that's happening in this particular case. You're the cheerleader here.

ReplyDeleteDavid, I think he means that you say housing prices are going down but the facts are contrary. Please address. Thanks.

ReplyDeleteDavid, you said

ReplyDelete" If you adjust for inflation the median sales price decline was statistically significant."

Median sales price in Arlington County was up 2%. Inflation, depending on if you are using PPI, CPI or another index, has been running at 2-3%. So "adjust[ed] for inflation the median sales price decline was" either non-existant or 1%. Are you saying a 1% decline is "statistically significant?"

"Are you saying a 1% decline is "statistically significant?" '

ReplyDeleteNo. But that was for just Arlington, the data I am talking about includes "Fairfax County, Fairfax City, Arlington County, Alexandria City, & Falls Church City, VA"

David,

ReplyDeleteSo you would say that there has been no price decline for single family houses in Arlington County?

There will be no soft landing in N. Va.

ReplyDeleteExpect real dollar price declines of 25% for SFH from peak real dollar price. Even greater real dollar price declines for condos.

David said

ReplyDelete"There will be no soft landing in N. Va. Expect real dollar price declines of 25% for SFH from peak real dollar price."

You still believe that, even though you have absolutely no proof so far...

"You still believe that, even though you have absolutely no proof so far..."

ReplyDeleteI have no proof. Just really strong evidence. An example of the evidence is the presented graph. It will not just magically stop at 0% price appreciation.

The best thing is that in a matter of a month the discussion has changed from "housing prices are going to go up" to "a 1% decrease isnt that bad".

ReplyDeletePeople truly dont understand how bad this is. My sister bought a 250k house in wisconsin, family income 100k. If their house price drop 10%, they are down 25k. That is not that dramtic for them. If they had to, they could come to the table with 25k. If your 800k arlington home drops 10% you have to bring 80k to the table. That is more than most people make in a year here. You just dont recover from those types of losses. Keith, nice post on statistics. Errors in statistics are one of the biggest causes in financial mistakes!

Bob

" It will not just magically stop at 0% price appreciation. "

ReplyDeletePrces will not just magically drop 25%.

See how persuasive you are?

""Maybe prices really will just level off for the next five years."

ReplyDelete-Catalyst, on Bubble Meter, June, 2005

"Stock prices have reached a permanently high plateau."

-Irving Fisher, renowned Yale economist, September, 1929"

Superficial similarity = fate

it must be relaxing to be so simple-minded.

Bob, of course prices are going to be flat or experience a decline for a while. I don't disagree with that at all. And it is certainly possible that they may decline significantly. All I am saying is that there has been no actual evidence of that to day in the Arlington market. But I don't disagree with your general thrust in the least--anyone who bought with a short term mindset in NoVa in the last couple of years is in for trouble. But close-in houses, over a moderately long time horizon, are unlikely to be a money-losing proposition.

ReplyDelete"My response: Assume a house that sells six years ago for $200K has appreciated by 100%. That house is now worth $400K."

ReplyDeleteThis is wrong, but nice of you to be obnoxious while being incorrect.

If a 100,000 house appreciates 10% from 2000 to 2001, then it is worth 110,000 in 2002, right? Then if it appreciates another 10% from 2002 to 2003, then it is worth 121,000 in 2003. Then if it appreciates 10% from 2003 to 2004, then it is worth 133,100. See, there is a little thing called "COMPOUNDING"

You're welcome!

"might be better to wait a few years, rent, and make more money on other investments"

ReplyDeleteHow is the possible when the general bubblehead philosphy states that there will be either 1) DOOM or 2) GLOOM across the entire national economy.

See what has happened in the stock market over the last month for evidence of your own theory coming true.... unless of course it contridicts the other part of your hypothesis; that "other investments" are a better place for your money right now. Oh wait, you have a self-defeating circular argument on your hands! nevermind.

Let's try to explain what is going on in NoVA. NoVA inventory is up 4X YoY. Inventory in Loudon is up almost 12X YoY, last I heard. Nominal NoVA median prices have been relatively flat for 12 months, but nominal prices in Arlington have increased 9%. Days on market has increased a lot, but it still isn't bad.

ReplyDeleteThis can all be explained as a flight to quality. When inventory was low, any old piece of crud sold for an exhorbitant price. There wasn't much differentiation. With inventory high, the best properties (eg. short Arlington commute) would be expected to hold their values, at least until the bitter end, while less desirable properties will simply not sell until the sellers finally cave in and signficantly lower prices. Here's another way to put it: if NoVA prices have been flat, but Arlington has increased 9%, then the REST of NoVA (minus Arlington) must have experienced price drops. It's very possible that Arlington will experience a soft landing, for example, while Loudon will not be so fortunate - it won't affect everyone equally.

I'm interested in opinions on the 32% decrease in sales. Does that represent only the speculators who have pulled out and the "normal" buyers have kept right on buying? Have we reached the end point where the normal buyers just can't afford to buy anything even with an exotic mortgage? Interest rates? Buyers getting wary?

Likewise, is the inventory increase just due to speculators dumping their properties, or are there simply more "normal" sellers than normal buyers due to the sales decline?

If we could answer these questions, we'd have a better shot at predicting what will happen. I think average days on market and inventory growth are the key indicators to watch, since they are predict price erosion.

Anon 8:50 AM,

ReplyDeleteJust where am I wrong?

You are looking at compounding GAINS while my post looks at compounding LOSSES, the point of my post being that 100% cumulative appreciation can be erased by a 50% cumulative depreciation, a rule which ceteris paribus holds for any asset over any span of time (e.g. whether said appreciation takes 10 years, and depreciation takes 5 years)

And...when I say "Assume a house appreciates by 100%" that means assume a house appreciates by 100%...

Again...you have proved my point for me re: mathematical illiterati, and I really do thank you. The combined effect of you math whizzes will greatly enhance my home-buying power in 2008 and 2009.

"If a 100,000 house appreciates 10% from 2000 to 2001, then it is worth 110,000 in 2002, right? Then if it appreciates another 10% from 2002 to 2003, then it is worth 121,000 in 2003. Then if it appreciates 10% from 2003 to 2004, then it is worth 133,100. See, there is a little thing called "COMPOUNDING""

ReplyDeleteAnd if the house price then drops 30% the next year, then it's worth 93,170, which is 7% less than it was worth in the first place. See, because 30% of 133,100 is more than 30% (or even 10% compounded three times) of $100,000.

You're welcome!

Basically, prices are dropping - just a matter of degree (and for how long) at this point.

ReplyDeleteAnon 8:54,

ReplyDeleteYou reveal yourself quite clearly to all on the board when you assume that "other investments" are, by necessity, a subset of the "national economy". I am one of those that predicts what financial ignorami such as yourself might call "doom and gloom" for dollar-based investments. The trick is knowing how to take advantage of those investments that are completely uncorrelated with a currency that is structurally unsound, particularly avoiding assets undergirded by absolutely mindblowing amounts of debt securitized and hedged by even vaster sums of derivatives. This is the state of dollar denominated paper assets, including stocks, bonds and housing (through the MBS market, underwritten by FNM and FRE).

A corollary to your attack on DC_too might be a question to you, and others who think like you:

Your financial world is limited to a paper currency printed at will by a country with multiple billions of annual trade and budget deficits, no industrial base and an indebted populace, why would we take financial advice from you?

"Again...you have proved my point for me re: mathematical illiterati, and I really do thank you."

ReplyDeleteI spelled it out for you on the way up, now I'll spell it out for you on the way down: A house worth 100,000 in 2006 experiences a 10% drop in value between 2006 and 2007: The house is worth 90,000.

Then it experiences another 10% drop the following year: 81,000. See? It falls slower than it rises due to the magic of compounding. Maybe you'll catch on if you squint your eyes more.

"am one of those that predicts what financial ignorami such as yourself might call "doom and gloom""

ReplyDeleteThese are the words of this forum's moderator and the Wash Post Express, which quotes him regularly. These aren't my words. Read the last two sentances again.... yes, they are true. (look it up)

Oh, and I'm not the person conversing with dc_too. You are so very presumptuous.

I have read this blog in the last few weeks with interest. We are in the position now to either rent a 3 bdr townhouse in Arl. for $2000/month or buy one (no money down, 10 year ARM) for $550K (they are the exact same model, but the for sale one is nicer inside (granite counters, etc.) Anyone have any advice? Even my RE agent didn't try to talk me out of renting, which really surprised me. She thinks prices will drop. OH, and we would prefer to move to a bigger place in 5-7 years.

ReplyDeleteRent - 50% cheaper than owning right now, and easier to walk away from, if need be. Take your time with buying. Look at all the inventory. What's the rush?

ReplyDeleteBill,

ReplyDeleteI have looked in this area for 3 years. Believe me I am taking my time. The problem is, these 3 bdrs only come up so often. They are very sought after. We made an offer on one in April and someone overbid us and paid full list price. (They are morons, but what can you do.)

Anon 12:09,

ReplyDeleteI am enjoying the straw man of compounding that you persist in putting up...but that doesn't impact my argument in the least. I concede that your ability to point out obvious facts with no relevance to an argument exceeds mine.

My initial post: "Assume a house that sells six years ago for $200K has appreciated by 100%. That house is now worth $400K."

Your response to that quote: "This is wrong, but nice of you to be obnoxious while being incorrect."

Your contention being that a $200K house that has appreciated by 100% over six years is NOT worth $400K. I have no response...such idiocy speaks for itself.

Lance, et al. Here is the type of data collection and analysis we ask of you in supporting your claims:

ReplyDeletehttp://bigpicture.typepad.com/comments/2006/06/housing_leads_t.html

When did this site get overrun by a horde of jerks?

ReplyDelete"Prces will not just magically drop 25%."

ReplyDeleteNo. Neither magically nor over night.

But the downtrend on the graph is clear.

It will not go down in one straight line either.

It will take a few years to drop 25%.

fritz,

ReplyDelete"When did this site get overrun by a horde of jerks?"

I deleted many of the comments in accordance with the blog rules.

The deletes occured against housingheads as well as bubbleheads.

"Your contention being that a $200K house that has appreciated by 100% over six years is NOT worth $400K. I have no response...such idiocy speaks for itself."

ReplyDeleteWhat? That isn't what is being said at all. You said that a 200K house that rose to 400K in six years rose at a rate of 100%, *when the topic of the thread is YoY trends*. YoY trending got it to double in six years - it was not as a result of a dramatic 100% increase all at once, but as a result YoY of compounded gains.

The thread is talking about YOY trending! YOY trending is compound by definition!

Where is that guy who says he lives in Rome? He must be back out on the town again tonight. LOL!

ReplyDeleteI'm the guy who lives in Rome. Good night here - Italy won their world cup match. Too bad about our guys.

ReplyDeleteI found an interesting report for everyone:

http://www.marketwatch.com/News/Story/Story.aspx?guid=%7B15CBFA40-B271-46D0-8731-88B1F2D1B0BC%7D&siteid=google

[Read this report, click on the link that says "Read the complete report," and then look at page A-8 or 8.]

This the kind of data all you anti-bubbleheads fail to cite in your arguments that DC real estate is not overvalued right now.

"When did this site get overrun by a horde of jerks?"

ReplyDeleteWho are you talking about and why are they jerks?

http://www.marketwatch.com/News/Story/Story.aspx?guid=%7B96064A61%2DB776%2D4BA6%2DAC72%2DEA43B55475BB%7D&siteid=mktw&dist=

ReplyDeleteWall Street's take on prominent housing builder.

David,

ReplyDeleteSo we understand what you mean by the use of certain terminology, what would charecterize a "soft landing?"

Thank you.

"So we understand what you mean by the use of certain terminology, what would charecterize a "soft landing?""

ReplyDeletereal dollar price declines of less then 25% from peak real dollar price

Thanks to those who posted links. Please use tinyurl.com (when it's working) to shorten your links. It's so simple, even a realtor can use it!

ReplyDeleteAnd on the more serious side, I highly suggest that you contact your friends and family, and tell them to lighten up on their stock holdings. If they take a tax hit, fine. It's a lot better than paying no taxes and losing a bundle. Start with people you know that are retired, although they shouldn't have much in stocks anyway. DO IT QUICKLY because you never know...we could have a Black Monday coming up soon if derivatives begin to unravel. And finally, when you tell your friends and family to sell, don't sound like their house is on fire...do it calmly and have sound arguments to back up what you are talking about...otherwise they won't listen to you.

Sorry to be off-topic, David, but I think it needs to be said. Protect the ones you care about.

Okay seriously, this guy is just yanking our chain right?

ReplyDeleteFirst of all you say

"So home prices are up more than 100% in the last six years. And now, for the sake of discussion, we are in for three years of 10% price delcines? So they're still up over 70%."

No, you are not up over 70%. In your example, for a house bought for 200,000 the values would be as follows

time 0: 200,000

time 6: 400,000 (100% appreciation, NOT annual appreciation, that would be a different calculation)

time 7: 360,000 (a drop of 10%, 40,000)

time 8: 324,000 (a drop of 10% or 36,000)

time 9:

ime 6: 291,600 (a drop of 10% of 32,400)

Now then, you now have a gain of 91,600, which in percentage terms is a 45.8% return, not bad, but also not the 70% you maintain. See if something goings up 100%, it only has to go down 50% to be back to the original value. Think about it.

Now, as for your 91,600 gain. This represents an ANNUAL rate of return (over 9 years) of .... 4.3% Now if inflation had risen at 4.3% over this same time (not saying it has) then your house would be worth exactly the price you paid for it 9 years ago. See why you factor in inflation now?

It becomes tedious to follow the discussion with multiple people using anonymous.

ReplyDelete" Anonymous said...

ReplyDelete"Prces will not just magically drop 25%."

No. Neither magically nor over night.

But the downtrend on the graph is clear.

It will not go down in one straight line either.

It will take a few years to drop 25%. "

Duh, no it won't. I'm as persuasive as you.

David,

ReplyDeleteDid you check DC's May data coming out from GCAAR:

http://www.gcaar.com/statistics/default.htm

The median YOY price has dropped for both Condo and SFH in DC. Price in Mongomery County is still sticky.

That is important enough to deserve a proper hard link.

ReplyDeletePdf document, DC Real estate has YoY declined.

We are on track for 15% real declines YoY by years end. The spring rally has failed, there is no spring rally, this is the silent spring.

Anon 5:56 :

ReplyDelete"This represents an ANNUAL rate of return (over 9 years) of .... 4.3% Now if inflation had risen at 4.3% over this same time (not saying it has) then your house would be worth exactly the price you paid for it 9 years ago. See why you factor in inflation now?"

Your calcs are relevant if you are an flipper ... Not relevant if you are a homeowner or even an investor(i.e., longterm buyer) because payment would stay the same ... effectively shrinking them by 4.3% per year over the period where you salary would likely be increasing by a similar amount (or your rents increasing by a similar amount if you are an investor.)

Btw, interesting article about how speculators have already pulled out ... and how despite this, prices are NOT expected to drop significantly ...

http://www.cbsnews.com/stories/2006/06/12/business/main1704608.shtml

(sorry, I prefer not to use TinyURLs because I don't want my email address spammed anymore than it already is!)

Another indication real estate in the District is alive and well:

ReplyDeletehttp://charlotte.bizjournals.com/washington/stories/2006/06/12/story5.html

Oh comeon, just 'cause Morgan Stanley recently announced a plan to inject $150M funding into a long-blighted neighborhhood in DC, it does not mean that there is *ANY* upside left in RE in DC. Haven't you heard? All that "close in" property is worthless. It is the land in Vienna VA that is invaluable!

ReplyDeleteNCRC Partners With Morgan Stanley

Morgan Stanley Commits $150 Million To NCRC's Mission

By Sean Madigan, Senior Staff Reporter

[http://washington.bizjournals.com/washington/stories/2006/06/12/story1.html]

The National Capital Revitalization Corp. has reached a deal with Morgan Stanley Real Estate that will inject $150 million into NCRC's projects over the next three years.

The Wall Street firm is committing the money through equity financing for projects such as the long-awaited, $125 million redevelopment of the Skyland Shopping Center, as well as several key neighborhood developments. If the projects generate profits, Morgan Stanley, NCRC and other members of the development team will share the proceeds.

"We are on track for 15% real declines YoY by years end. The spring rally has failed, there is no spring rally, this is the silent spring. "

ReplyDeleteWhy do you keep saying this? This does not include spring contracts, only spring closings. You make yourself look like an idiot.

The real estate agents are out in full force with their troll talk. RE is a stupid investment, especially now that we are at the top of the bubble looking down at six years of declines.

ReplyDeleteAnon 6:01 said:

ReplyDelete"Why do you keep saying this? This does not include spring contracts, only spring closings. You make yourself look like an idiot."

Sure, but the May 2005 numbers almost certainly didn't include contracts, either, so we are comparing apples to apples, and the apparent year-on-year decline in median sales price is real. Or are you suggesting that GCAAR, a realtors' association that "[Serves] the Business Needs of [ITS] Professionals," is publishing garbage statistics that incorrectly suggest anemia in the D.C. real estate market?

Anon 3:16

According to USA TODAY - DC is overvalued by about 40 PERCENT!

ReplyDeletehttp://www.usatoday.com/money/economy/housing/2006-06-12-home-prices-usat_x.htm

http://www.usatoday.com/money/economy/housing/2006-06-13-overvalued-markets-chart.htm

Where's the Roman guy to talk about how stylin' he is in Rome (NY)?

ReplyDeleteDon't worry about those USA Today numbers. What those media bubbleheads don't understand is the land supply is limited. Plus, there's a new housing paradigm in DC, when values never go down. Why? Because the federal government is spending a lot of money here.

ReplyDeleteAll's well here in DC. Values will just decline every else. Don't let facts and analysis get in your way of buying today!

"

ReplyDelete"Why do you keep saying this? This does not include spring contracts, only spring closings. You make yourself look like an idiot."

Sure, but the May 2005 numbers almost certainly didn't include contracts, either, so we are comparing apples to apples, and the apparent year-on-year decline in median sales price is real. Or are you suggesting that GCAAR, a realtors' association that "[Serves] the Business Needs of [ITS] Professionals," is publishing garbage statistics that incorrectly suggest anemia in the D.C. real estate market?

Anon 3:16 "

So, you admit that you messed up on your point about spring sales.