Subscribe to:

Post Comments (Atom)

Bubble Meter is a national housing bubble blog dedicated to tracking the continuing decline of the housing bubble throughout the USA. It is a long and slow decline. Housing prices were simply unsustainable. National housing bubble coverage. Please join in the discussion.

Nice.

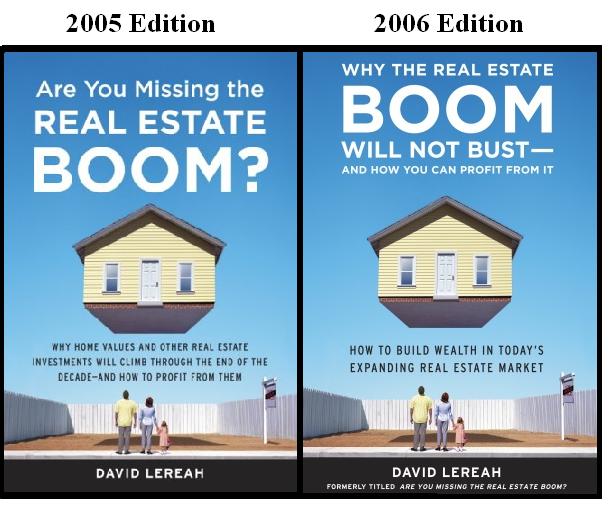

ReplyDeleteI wonder if the 2007 edition will be "How You Can Still Profit From a Busting Real Estate Market".

It is amazing to me that that man still has any credibility left at all.

Eventually, that house will fall on those poor people.

ReplyDeleteNow all they need to do is move the family under the house.

ReplyDeleteThat is in the works for the next edition.

Marinite said...

ReplyDeleteNice.

I wonder if the 2007 edition will be "How You Can Still Profit From a Busting Real Estate Market".

That's okay because noone even read the book, so it doesn't matter what the title is.

Look, the guy is a lobbyist. What do you expect him to say?

ReplyDeleteI was checking the stats for the David Lereah Watch blog the other night. In it, I found that someone from the National Association of Realtors had googled 'David Lereah' and found their way to the David Lereah Watch blog. Hehe!

ReplyDeleteva_investor said...

ReplyDelete"Look, the guy is a lobbyist. What do you expect him to say?"

... hmmm, does that make him part of that vast conspiracy? ... the housing industrial complex conspiracy that is meant to keep some people as a perpetual underclass? do you think maybe "W" himself or his trusty keeper are designing the cover of this publication ... and doing it just for the kicks to see how we respond to it ... ?

He is acting in his own self interest, and he is worried about his own investments. He believes that psychology can keep the market up, unless the fed continues to raise. I don't agree with him, and also the fed is continuing to raise. That makes him a liar if we do have a bust. And we are getting close.

ReplyDeletehttp://www.washingtonpost.com/wp-dyn/content/article/2006/06/21/AR2006062101735.html

ReplyDeleteWashington Post - "U.S. Losing Its Middle-Class Neighborhoods"

The floating house image is really interesting. The family watching it, as if they are thinking, "Gee how the f**k did our house get up there?" is even more telling. "There is nothing normal or natural about this state of affairs", this cover seems to admit -- "don't ask questions, just get on board." Some of the smartest people I know are completely deluded by this situation. They are not talking about how completely screwed up our world has become -- they have drunk this levitating-house-kool-aid. Sad, and scary.

ReplyDelete-- waiting it out in Boston.

Sounds familiar...

ReplyDeletehttp://tinyurl.com/g79ju

Most people shouldn't be allowed to publish books in this country, especially since others are forced at gunpoint to buy and read those books.

ReplyDeleteThe government should decide who can and who cannot publish books in this country. Clearly, this guy should be banned from expressing himself in writing.

ReplyDeleteBill said...

ReplyDelete"http://www.washingtonpost.com/wp-dyn/content/article/2006/06/21/AR2006062101735.html

Washington Post - "U.S. Losing Its Middle-Class Neighborhoods""

How interesting ... I was going to post the same link ... It expresses pretty well the economic divide that is occuring everywhere including DC ... and why the District and close-in areas are slowly but surely switching converting to "high class" neighborhoods where only those with the means can live. What you were calling "the paradigm shift" for DC.

Anonymous said...

ReplyDelete"The government should decide who can and who cannot publish books in this country. Clearly, this guy should be banned from expressing himself in writing."

H*ll no! We don't want no government grunt telling us what we should or shouldn't read.

The Church should decide!

"The Church should decide!"

ReplyDeleteThe Government AND the Church should keep us safe from predators like David Lereah. It is what the founding fathers would have wanted.

lets stick to the topic!

ReplyDeleteI never called anything a "paradigm shift." Those are your glorious terms.

ReplyDeleteI would say this is a wealth shift. One in which some in the middle-class have achieved the American dream of wealth through home ownership - or doing little to nothing to make a lot of money on paper fast (echoes of the late 90s stock bubble).

Unfortunately for these folks, they are living on credit and wealth that's recorded on paper only. They're heavily in debt to the banks (mortgages, car loans) and credit card companies to furnish these increasingly large homes in which they live.

What goes up, always comes back down - including the DC housing market. It's a matter of degree only at this point.

Bill said:

ReplyDelete"Unfortunately for these folks, they are living on credit and wealth that's recorded on paper only. They're heavily in debt to the banks (mortgages, car loans) and credit card companies to furnish these increasingly large homes in which they live."

I would agree with you were it not for the very real "extra" dollars flowing into the pockets of the residents of the Washington area because of the very real (and extra large) budget spending that is being concentrated more and more in this area. Even if you are not a direct beneficiary of the dollars flowing straight from the US Treasury into the pockets of many around here, you're benefiting from them receiving them because they are spending their dollars here too for the most part ... on clothes, restaurants, expensive grocery stores, cars, and even on that furniture you mention. The increased US budget is floating the local economy directly ... causing prices for housing to rise with it. You yourself say that you have plenty of money left over after paying the rent. Money you are using to invest or whatever. That is your right to decide what to do with it ... But, the long and short of it is that if you wanted to buy you could ... The local economy supports the higher real estate sales prices ... easily. That may not be the case in areas where the local economy is unchanged since the late 90s, but that is the case here. If you're waiting for a bubble to burst here, you are waiting in vain. Going back to pre-2000 prices is as likely as your salary going back to what it was pre-2000. And it's salaries (and general wealth) that drive prices in a rational and real market ... which is what DC's market has for the most part been. Not completely, I agree that some increase is due to speculative buying. But these buyers have retreated from the market and the slight decrease in prices is already being felt. Just don't hold out for a large decrease in prices ... not in this area with all the money floating around out there.

Lance,

ReplyDeleteHow much longer do you think that money can keep flowing to this area via the federal government? Through the current administration's term? The next?

Our federal deficit is enormous, and we have looming medicare and social security problems. The government is riding high off of easy credit just like a lot of irresponsible consumers.

Eventually, that debt needs to be repaid. The longer we wait, the more drastic the solution will have to be.

My $0.02.

For 2007 how about:

ReplyDelete"The boom has busted, but the busting of the boom was unforeseeable and was the fault of booming bubble talk by the media"

or

"Why the busted real estate boom is doomed - a guide to real estate serfdom for boom-time buyers for the next decade: You better learn to love Alpo"

"Through the current administration's term? The next?"

ReplyDeleteThe size of the US federal government ALWAYS increases, without exception. The republicans talk about "smaller government", but the facts are that every administration, including this one, has increased the size of the federal government.

Those in disagreement should check into the facts before sounding off here. (Because it is a verifiable fact)

Hey guys. This is one of the best articles out there from yesterday's WSJ. David you should do a story on this. People are now realizing that real estate will return BELOW average returns when compared to other forms of investment.

ReplyDelete------------------

Don't Blame the Latte: The Real Reason

You're Not Saving More Is Closer to Home

June 21, 2006; Page D1

It's time to put our house in order -- and maybe the garage, too.

The U.S. savings rate has fallen sharply since the mid-1980s. In fact, last year, it was negative for the first time since 1933.

At first blush, this collapse in the savings rate seems puzzling. Our incomes have climbed at a healthy clip over the years, easily outstripping growth in spending on key items like food and clothing.

So why do we find it so tough to save? We can't, it seems, blame it all on morning lattes and evenings out. Instead, the big culprits are our two largest expenses: The roof over our head and the cars in our driveway.

• Signs of struggle. Some pundits have argued that the savings rate isn't as low as the official statistics suggest, or that Americans don't need to save so much because they are wealthier than ever. But when I look around, I see plenty of signs of financial distress.

A study sponsored by Putnam Investments estimates that seven million retirees have chosen or felt compelled to return to work. A Pew Research Center survey discovered that 20% of baby boomers had provided financial help to a parent within the past year. Families are also finding it tougher to pay for college, with College Board data showing a 194% increase in annual borrowing through college loans over the past decade.

All this suggests folks are struggling to make ends meet. But why? Consider a new study from the U.S. Department of Labor titled "100 Years of U.S. Consumer Spending." The study draws on the Bureau of Labor Statistics' consumer expenditure survey.

It might seem like Americans spend too much on clothes, eating out and entertainment. In reality, however, the portion of our spending that's devoted to food and apparel has fallen sharply over the past century.

Tobacco and booze also account for a shrinking share of spending. Meanwhile, the slice of our budget that goes to entertainment and health care isn't much changed from 40 or 50 years ago. Indeed, if you look at all these categories, you might imagine families have ample financial room for maneuver.

• Road to ruin. Yet we struggle to save -- and the blame seems to lie with two other expenses, transportation and housing.

Our transportation spending jumped sharply in the 1960s and has remained high ever since, accounting for more than 19% of spending in 2002-03. It's easy to see why: The number of passenger vehicles has leapt 270% since 1960, far ahead of the 86% increase in the adult population. We now have one car, van, pickup truck or sport-utility vehicle for every adult.

"The automobile is no longer a luxury item," says Michael Dolfman, the Bureau of Labor Statistics' regional commissioner in New York and co-author of the new BLS study. "Cars became a necessity to get to work," with working couples often needing two cars.

Meanwhile, housing expenditures have climbed fairly steadily over the past century, and our homes now claim a third of our spending.

More families are buying houses, more folks are purchasing second homes, and houses are getting bigger. According to the Census Bureau, over the past 25 years, the number of second homes has jumped 95% and the size of the typical newly constructed single-family home has ballooned 40%.

• Saving ourselves. Put it together, and houses and transportation accounted for 52% of all expenditures in 2002-03, up from less than 41% in 1950.

You probably need to have a car, and you've clearly got to live somewhere. Still, it strikes me that housing and transport expenses are ripe for cutting, if only because they are such plump targets.

But how are you going to cut back? Consider this: We may be spending more on cars and homes, but we are also purchasing cars and homes that are far more luxurious.

"The trend has been to buy the most house you can afford, rather than the amount you need," notes Sophie Beckmann, a financial-planning specialist at A.G. Edwards in St. Louis. "It's the same thing with cars. You see a lot more luxury cars on the road. While you can get by with a $20,000 car, people buy the $40,000 SUV with the leather seats and the TV. There's a lot there that's discretionary."

Indeed, if you're willing to skip the heated car seats and the third bathroom, you would probably still be living better than your parents did -- and you will free up money that can be saved.

This suggestion may puzzle some readers. Sure, cars might be money losers. But houses appreciate over time, so shouldn't you buy the largest home possible?

That might have been true during the recent housing boom -- but it isn't likely to be true over the long run. Since 1975, home-price appreciation has been modest, averaging just two percentage points a year above inflation.

Admittedly, you could goose your home's return with the leverage from a mortgage. You also, however, have to factor in the mortgage's cost, plus all the other expenses of homeownership, including maintenance, property taxes and insurance. The bottom line: Once you deduct those costs, you could probably amass far more wealth by purchasing a smaller home and then sinking the extra money into your 401(k) plan.

"lets stick to the topic!"

ReplyDeleteThe topic here, in general terms, is David's notion that Mr. Lereah is a threat to many people in this country. The notion is that by expressing himself, Mr. Lereah causes quantifiable damage to innocent people.

THAT is the topic. We need protection from men like Mr. Lereah.

I hope David Lereah is exposed for the snake oil salesman that he is.

ReplyDeleteaw man, somebody good w/ photoshop get to work! i'm thinking a scene similar to the wicked witch's demise in Wizard of Oz, feet coming out from under the house and maybe a little arm clutching a teddy bear to add that whole family tragedy thing. classic.

ReplyDeleteProtect us from this man's thoughts! HELP!

ReplyDeleteJim A said:

ReplyDelete"Now neither my (government) salary nor anybody I know's salary has nearly tripled since '99."

Granted mine hasn't doubled since then ... more than doubled, yes, but not tripled ... Alos, I know lots of folks who through job hopping have indeed tripled their overall income ... perhaps not directly through "wages", but via bonuses, stock options, etc. You're a government worker and wouldn't have seen that happen to your salary because your salary (when you add the long term government benefits to it) was relatively high to begin with ... And ALL administrations over the last 25 years or more have been shifting more and more of the workload to us contracting folks who get paid more in the shortterm, but don't get the longterm health and pension benefits that are so costly to government (and the taxpayer) in the end. Overall, enoough folks --- not all --- are making enough more in this area to justify most of the increase in selling prices.

Maybe that should be the title of this blog ...

ReplyDelete"Has the bubble bursted for those who can't keep up?"

Lance thinks he is so smart because he thinks his salary is big. That makes him smart, right? He doesn't understand that in arguments like these, ancedotal evidence using yourself and your peer group as examples is baseless drivel. Look to the median household incomes, look to the historical return of homes (3.4% - just ahead of inflation) to assess the situation.

ReplyDeletePeople who are doing all right always feel they are smart. In truth, with perspective they would understand how much better they could have done with other investements. Explanation - if you were 80 to 90% leveraged in the equity markets (the way lots of folks are on their homes), a return of 15 - 20% per year would be nothing to get excited about because at that level of risk returns need to

be that much greater.

http://bigpicture.typepad.com/comments/2006/06/why_the_real_es.html

ReplyDeleteInformed discussion of housing market and the effects of mortgage equity withdrawal on GDP.

Facts, data, informed analysis... Try it sometime, Lance. People might then take your real estate cheerleading/lifestyle counseling seriously.

This book is going to be come a collectors item. A bit like "Dow 36,000".

ReplyDeleteAlso, it ironic I think, but the picture on the cover to me looks like an unfortunate family confronted with homes that are now out of reach.

anon (8:38) Your "return" numbers are off due to 2 reasons (at a very minimum)... (1) the returns you quote are calculated on the total average selling prices of average house at any given time. The power of leverage is ignored in that calculation. If you pay cash for a $100K house and it doubles in 10 years time, you have made 100% on it over the 10 year period. If you instead put $10K down, and it doubles in 10 years, you have made somewhat more than "$190K less financing expenses" ... i.e., your return is approaching 1,800% for your $10K investment ... over a 10 year period. (2) again the return calcs you quote are for an average house in one year as compared to an average house in another year. The "average" house in 2006 in the DC area might be a house out in someplace like Gaithersburg. The average house in 1906 would have been a house in Logan Circle or Dupont Circle. Compare the prices of averages houses in either of these two neighborhoods, and you'll see that they are MUCH higher than the average price of a house in Gaithersburg that is being used as the current value of the "average" house in calculating appreciation. Jeez, I'm starting to realize why you're still not homeowners, you are shooting yourselves in the foot by misinterpretting everything out there so that it validates a "chicken little" attitude. Look as the big picture ... most times that will tell you more than the stats which as well all know can be twisted to tell you whatever it is you want to hear! And, it's obvious you want to hear that the sky is falling because that validates your prior indecision. It unfortunately also enables your current indecision.

ReplyDeleteMy son makes 130k per year and is renting. He is not stupid, at age 26, and realizes that there is a bubble of Ghostbuster proportions.

ReplyDeleteAnonymous said...

ReplyDeleteMost people shouldn't be allowed to publish books in this country, especially since others are forced at gunpoint to buy and read those books.

The government should decide who can and who cannot publish books in this country. Clearly, this guy should be banned from expressing himself in writing.

Anonymous is on the right ironical track but heading the wrong direction. The government should prohibit people from reading or writing any blog that criticizes stupid books.

Gary Anderson said...

ReplyDelete"My son makes 130k per year and is renting. He is not stupid, at age 26, and realizes that there is a bubble of Ghostbuster proportions."

And your son's relatively high salary given his young age and relative inexperience is a large part of the reason why house prices have ballooned in this country and this town in particular. Since the Reagan years, we have had a growing economic divide that is reducing the size of the middle class that has been the backbone of this nation and pushing people to either one side of the wealth divide or the other. Prices are up nationally because there are lots more young people like your son earning the level of salary that once took years of experience to acheive. They are up even more so relatively higher here because a new national elite based on politcal power that is forming.

Um... this isn't news. The current edition of the book came out four months ago.

ReplyDelete" Um... this isn't news. The current edition of the book came out four months ago."

ReplyDeleteI know but David Lereah deserves to be exposed for his shameless cheerleading.

MSM where are you?

Gary Anderson said...

ReplyDelete" My son makes 130k per year and is renting. He is not stupid, at age 26, and realizes that there is a bubble of Ghostbuster proportions."

Gary I think you have just furthered Lance's point. If your son makes that kind of money at the age of 26, doesn't that say alot about the overall wealth in this area? Now your son may very well be renting. But I am sure he is spending that 130K somewhere. And that further boosts the local economy. The first check he writes every month will be his rent. And with his salary, he is unlikely to quibble about the rent. One other thing. Outside of SF, Boston, LA, and San Diego, what other area is likely to offer your son a similar salary? And the aforementioned cities are just as expensive as here. And if your son is benefitting from having a security clearance, the ONLY city that has jobs in that range for his age and experience is here.

For every 26 year old in the DC area making 130K, there are at least 300 who makes less. Your son is an income anomaly.

ReplyDeleteDavid wrote:

ReplyDelete"I know but David Lereah deserves to be exposed for his shameless cheerleading."

Agreed.

Jim a wrote:

"How about a book titled Real Estate Fall down and go BOOM with a picture of six legs coming out from underneath the house, wicked witch style."

Or perhaps David Lereah should write a second edition of Jim Cramer's book You Got Screwed!, specifically for the real estate market (...since Cramer was a cheerleader for the tech bubble and Lereah is a cheerleader for the housing bubble).

all right smart a$$e$, check out this link:

ReplyDeletehttp://www.bls.gov/oes/current/oes_47900.htm

Lance simutaneously tells people to look at the "big picture" while deriding others for doing the same thing, as in: historical return on stocks = 11%, historical return on homes = 3.4%

ReplyDeleteAnd I am not undecided - I am completely confident that now in this current market, buying a poor decision and renting is cheaper.

And the chicken little comparison is funny too - chicken little is afraid for no reason. Smart savers/renters are not afraid.

By showing us that $50K is the mean (as in average) salary in Washington-Arlington-Alexandria, DC-VA-MD-WV (according to the Occupational Employment and Wage Estimates link he provided) Lance thinks he made his point. In fact, he just proved ours....

ReplyDeleteThey need and ARM up to buy that house. Otherwise it out of reach.

ReplyDeletelook through the managerial and other exec types positions ... as they disproportionately make up the new buyers in the District and surrounding areas ... look at their wages ... don't factor in the 17 yr old working at Mickey D's and living at home who helps bring down the average ... Better yet, compare this medium income to areas in the country that haven't experienced such increases in house prices as we have.

ReplyDelete"return on stocks = 11%, historical return on homes = 3.4%"

ReplyDeleteIf having a home of your own comes down to these two metrics, then you aren't a candidate to have a home of your own. You'll never enjoy the intangible, human aspects of having a place of your own with that "3.4%" number rolling around in your head.

Keep on renting, enjoy your stock portfolio AND your apartment. What is the big deal?

Oh come on Lance, we all know that DC is a blue collar town!

ReplyDelete11% vs 3.4%

ReplyDeleteThe 3.4% ignores the "value" of living in the house - i.e. rent savings.

In the alternative, this figure does not account for "leverage".

Comments?

look through the managerial and other exec types positions ... as they disproportionately make up the new buyers in the District and surrounding areas ...

ReplyDeleteso i guess all the managers are going to buy everything then, because we all know managers are in the market for a $300K studio condo!

Does Lance even think about these things before he sends them out?

ReplyDeleteAccording to data from the pages he provided, average wage increase incrased from $45,860 in 2003 to $50,000 in 2005: a 9% increase

In the same time period, how much did homes appreciate?

VA Investor,

ReplyDeleteThat's the big question. What is the intrinsic value of owning? What is that piece of mind worth? It'll be different for everyone.

To me, if I'm saving over $1500/month renting rather than owning, that's too steep a difference. I'll paint and put up shelves to my hearts content in the rental because for less than one month's "piece of mind" I can restore the rental back to the same condition I found it in. And in the meantime I'll enjoy the colors I want the whole time...

My $0.02.

Actually NOT thinking of my home as an 'investment' frees me to enjoy the intangible, human aspects of having a place of your own. So does having an affordable mortage, which is made possible by the large down payment I saved by renting.

ReplyDelete"It'll be different for everyone."

ReplyDeleteIn all seriousness: having said that, why do you put time, thought, and effort into undermining the personal decisions of others? It appears as if you are looking for affirmation of your choices from strangers on the internet.

Like I said; enjoy your healthy gains on your stock portfolio and enjoy your apartment too. What is the big deal?

mytwocents,

ReplyDeleteI am not talking "peace of mind", but actual dollars. The cost of rent is NOT included in the 3.4% figure.

ex. 100K purchase price. Pay cash.

appreciation 3.4% = 3,400/yr.

imputed rent $600/mos =7,200/yr

REAL RETURN = 10.6%

For a rental, the return is higher due to leverage and tenant paying your mortgage off.

EX: 100K purchase price

30K downpayment

Breakeven cash flow.

3.4% on 30K = over 11% and tenant pays off your mortgage. Plus depreciation deductions.

The mean for Washington DC is a little higher at 59K, but again still not high enough for someone in their 20's (such as myself) to purchase a 400K home.

ReplyDeletehttp://www.bls.gov/oes/current/oes_dc.htm#(2)

People,

ReplyDeleteIs there anyone out there willing to acknowlege the real return on RE? I've had this discussion with "financial planners" for 20 yrs. All there models assume a VACANT house.

I meant "their"

ReplyDeleteI needed to be a homewoner because of intangible reasons. I bought a house in the beginning of 2005.

ReplyDeleteMy big mistake was to follow my realtor's advice and buy the "perfect"

house by spending as much money as I could afford (within reason: with a fixed-rate mortgage).

Renting is not an option for me for psychological reasons, but I could have been quite

happy in a 450K house instead of 600K.

Now: I have a tighter budget than I would like, and a nicer

house than I really needed, and in addition, I am watching real estate blogs with dismay

as I contemplate the possibility of seeing my hard-earned savings diminish if prices

don't at least keep up with inflation. I have actually started resenting my house!

People like me won't show up in foreclosures, but it doesn't mean that they're happy!

Lance,

ReplyDeleteSorry I ran the numbers last year and moved to Texas. I lived in Vienna, made deep into the GS-15 range as a contractor (with stock & options) plus a full 20-year military retirement to boot. I bought (dumbest thing I ever did) in Vienna very near where I sold in 2000 when I left the area. Got a huge mortgage and an hour commute. Plus personel property tax, VA state tax, and huge property tax due to the outlandish value of my home. After a year wife & I did the numbers and I put my resume out the next day. I found a great job in Texas. When my old employer asked how much I needed to stay I replied."Pay off my mortgage or double my salary." I moved. Managed to sell in less than 30 nail-biting days for 18% more than I bought - and my new company picked up the realtor fees & move. Today my old house in DC would not sell for what I bought it for. The buyers who bought it are underwater - they did an 80-10-10 fancy deal (I don't know specifics - the money showed up). Our old friends say they are already scared and still have temp. window coverings up. I expect them to go under in a year or two.

Now tell me again why its so good to buy now, into a declining market? Rental for my old house would be at least 50% of buying in the same school district.

The 3.4% figure is not a return on investment figure, it is a historical appreciation figure.

ReplyDeleteIt also is meant to apply to homeowners, not those who are landlords. You have to live somewhere so you can't say rent is a cost and a mortgage is 'free'- especially since the early years of a mortgage are almost all interest payments.

The 3.4% figure is not a return on investment figure, it is a historical appreciation figure.

ReplyDeleteIt also is meant to apply to homeowners, not those who are landlords. You have to live somewhere so you can't say rent is a cost and a mortgage is 'free'- especially since the early years of a mortgage are almost all interest payments.

Anon,

ReplyDeleteThink some more. You are not getting my argument. 3.4% assumes a VACANT HOUSE.

The real question is why is Va_investor trolling the site? Why is anyone who "believes" all is well in the real estate world trolling RE bust sites? I imagine that is is because they want to debate with people like us to make themselves feel more secure about their decision to invest in the DC market. Because if they truly believe the dc market is good why would they waste their time reading the nonesense that comes out of our heads about the dc RE market.

ReplyDeletebuffpilot, thanks for being honest. Most homeowners on this blog are not.

Bob

va investor - in your 11:46am post you said "The 3.4% (long-term appreciation rate for real estate) ignores the "value" of living in the house - i.e. rent savings."

ReplyDeleteIsn't the average 2006 homebuyer paying a monthly mortgage tab greater than the amount of rent they could have paid? In other words, isn't there really no "rent savings" for 2006 buyers and actually "rent premium" being paid to the landlord (the bank)? And if so, doesn't this "rent premium" at least partially negate the 3.4% long-term appreciation benefit?

"Today my old house in DC "

ReplyDeleteLOL! He says he bought in Vienna, VA, had a horrible commute, horrible personal property and RE taxes, and then says "my old house in DC"?!

Vienna is not DC. There is a BIG difference. Like DC or not, VIENNA IS NOT WASHINGTON. Why don't you just say your old digs are in Gaithersburg. Same difference, right?

Buffpilot,

ReplyDeleteThe people who bought your old home were not responsible buyers. If they had to do a 80-10-10 and live at least a year so far with temp window treatments, then they bought more of a house then they could afford. I have NEVER said people should be irresponsible buyers. I have simply said three things in respect to the subject of this blog (1) don't expect prices in general to fall by 50% as most doom and gloom bubbleheads are claiming will occur,(2) "returns" on a home are not simply monetary ... pride of ownership and the socio-economic position that comes from owning one's own home are intangibles that all the money in the world cannot be substituted for, and (3) if you are buying a home to be used as a home (i.e., not an investment) then whether the value goes up 10-15% or down 10-15% or up 100% and then down again 50% in the next 2 -3 years shouldn't matter one iota 'cause what matters is that you can afford to stay AS LONG AS YOU WANT in your home. No landlord can kick you out because he/she wants to sell, move in themselves or whatever. (Again, I am assuming you were responsible and only bought what you could afford.) That is ALL I've been saying.

I am glad that you are happier in Texas with the larger home. We each have different wants in life. Personnally, as much as I love Texas and the Texans whenever I visit there, I couldn't live there. I have lived in similar areas, and for my personal needs I'd rather have the much smaller house but the ability to walk out my door and choose between a hundred and one sidewalk cafes within a 15 minute stroll. To each his own ... And that is the beauty of our free market system. Prices allocate what is available.

Any "rent premium" would be time limited due to inflation and would not offset the 3.4% but may slightly decrease the additional 7 or 8%. Less, of course, a factor that accounts for the tax-preferred treatment of mortgage interest and real estate taxes.

ReplyDeletei.e. mort. of 2100 equals 1500 after taxes.

VA Investor,

ReplyDeleteI think I get what your saying. The crucial part right now is the "break even" cash flow portion. Let's grant 3.4% asset appreciation.

Right now, with home pricing so high, it's hard to buy and have a mortgage price approximately equal to the rental price.

At one point I considered buying and renting with a negative cashflow because that 3.4% acts as a sort of buffer. Though the key is cash flow, that appreciation doesn't generate real cash unless you refinance all of the time and that increases the cost of capital.

As for leverage, the downpayment needs to get exceedingly larger to have the rent carry your mortgage payment when rent is much less than equivalent cost to own. Therefore, there's a larger opportunity cost on the downpayment cash and leverage is similarly reduced.

This all assumes you're buying a property to rent it out.

My $0.02.

mytwocents,

ReplyDeleteIt gets complicated. All I am, basically, is that the 3.4% assumes a vacant house (no rent or rent savings) and cannot be fairly compared to stock returns. Rent or imputed rent is like getting a dividend on top of your 3.4%

Financial planners can't or won't understand this.

Sorry about the rant. Yes Vienna is not DC, its just apart of the entire area - and a very desirable place to raise kids. I have 3. I have lots of friends who retired (83-85 Reagan buildup officer cohorts) who found 'good' jobs in DC, bought to settle down and found they can't live there. Taxes are crushing (and higher in DC than NoVA), commutes are longer, and just plain old day-to-day living much harder than when I was assigned here in '97-00. Cost of living is unbelievable even doing major shopping at the BX. Living in DC itself was never an option becuase the schools are atrocious and not getting better - and I could not afford the $30K+ for private (3 kids). Worse I could not find a doctor to take Tricare (military insurance in the area), had to go to Bethesda even for the most minor stuff and that killed a day for my wife and had to count on friends to watch the kids coming home from school since you could never count on gettinig back in time and I couldn't cover.

ReplyDeleteLance- what I was trying to convey, obviously poorly, that you cannot live on a median income (roughly $55K)an buy into the place. Heck its tough to even survive renting. I could not hire one person from outside the area - I had to recruit from other companies, PhDs who didn't make tenure, and from recent layoffs elsewhere. People outside DC just laughed at me - even when I offered 10-20% pay increases. They got on realtor dot.com, check commute times and laughed. If you got in in 99-00 (or before) your golden. But if not your screwed. The collapse will come and DC and area will take a big hit.

As for the living, I live within walking distance of TCU, shops and eateries. I have a 15 minute commute and its 15 minutes to downtown. 2 of my kids can walk to school, with bike trails and parks all around. I see my kids during the workweek, help them with homework, and we eat dinner together (instead of showing up burnt out at 7pm and putting the youngest to bed). I agree with you about all the intangibles, but they ALL improved when I left DC, including my bottom line.

Are you married with kids? That makes the DC life look far different. (yea - If I was 25 & single I would be having a grand time in a small rental chasing all the skirts, but that time is long over).

All your points are well taken, but this is really no longer true: "Taxes are crushing (and higher in DC than NoVA),"

ReplyDeleteReal property taxes in DC are falling, (deliberately, by design of the DC government) and there is no personal property tax. Sales tax is high, but if you own a house in Vienna proper, you're paying state AND local taxes which combined are higher than taxes on a place of comparable value in DC. Figure less than $2K on a home with an assessed value of around $500K.

Not that any of this matters to you now. :-)

Once again, Lance shows that it's Groundhog Day for him, latching onto one of the worst and oft-exploded explanations for the DC bubble.

ReplyDeleteIf DC incomes and those big government budget explained the rise in housing prices, then they would also drive rents. The fact that housing prices have risen IN RELATION to rents is what demonstrates the bubble and the fallacy of Lance's awful argument.

This has been pointed out to Lance, he has no reply, and he keeps repeating the same obviosuly wrong argument over and over. Lance is not thinking. He's parroting a comforting mantra precisely to avoid thinking.

"pride of ownership and the socio-economic position that comes from owning one's own home are intangibles that all the money in the world cannot be substituted for"

ReplyDeleteAside from the terrible sentence structure, is Lance really claiming that these things have infinite value, or at least greater value than everything else on the planet?

anon 2:29,

ReplyDeleteYou're telling me that property tax on a $500K house in DC is $2K??

That would make a millage of 0.4. Vienna was 0.4, Fairfax Cty 1.00 and VA 1.03 (last years data) total $2.43/$100 assessed value (usually 10-20% lower than sale price) or about $12000/year in taxes.

I don't believe you tax figure is right but I bet that we are doing an apples-to-oranges comparison. :)

BTW, millage in Fort Worth 3.07 for comparison, but the house costs a lot less so I actually pay less tax, especially with the homestead deduction.

Lance - "I have NEVER said people should be irresponsible buyers."

ReplyDeleteYes, but Lance has claimed that the price apreciation driven by all that irresponsible buying in late 2004-2005 won't go away.

"don't expect prices in general to fall by 50% as most doom and gloom bubbleheads are claiming will occur"

And in other contexts, Lance has also said he doesn't expect a 30% decrease, either. How much of a decrease does he expect? Would he care to commit? And are we talking real or nominal dollars?

"If you pay cash for a $100K house and it doubles in 10 years time, you have made 100% on it over the 10 year period. If you instead put $10K down, and it doubles in 10 years, you have made somewhat more than "$190K less financing expenses" ... i.e., your return is approaching 1,800% for your $10K investment ... over a 10 year period"

Lance conveniently ignores the downside of leverage. If you put 10K down, and the value of your house drops 10K, you've lost 100% of your investment. If you'd put 100K down, you would have lost 10% of your investment. Leverage raises the variance of your returns.

And when that variance bumps up against solvency constraints, which happens when the high-leverage approach is used as an affordability mechanism..so people start having to sell...and demand for housing is inelastic...so then increases in inventory (especially beyond 6 months) generate large price decreases to clear the market.

As for Lerah, who cares? He was a spokesperson for a sales organization. I really don't blame Lerah and realtors for any of the bubble. Realtors have always tried to sell houses by any means necessary, even during non-bubble periods.

ReplyDelete") or about $12000/year in taxes."

ReplyDeleteOh, no. Taxes in DC are nowhere near this. The city provides a $60,000 deduction from the assessed value of the property. This is called the "Homestead Credit". It also caps tax increases year over year at 10%. So even if assessed values climb quickly, the tax rate cannot jump more than 10%.

Granted, that 10% is still pricing a lot of people out of homes they've been in for a long time.

Here is a sample YoY tax assessment, taken directly from the searchable property database at DC.gov: (figures are rounded)

2006 Assessed value: $291,00

2006 Taxable assessment: $195,000

2007 Assessed value: $499,000

2007 Taxable assessment: $215,000

Here are dc's tax rates:

ReplyDeletehttp://otr.cfo.dc.gov/otr/cwp/view,a,1330,q,594394.asp

$0.92 per $100 for residential property

So, taking the sample property listed above:

Assessed 2007 value: $499,000

Taxable 2007 value: 215,000

less $60,000 deduction: 155,000

/100 : 1,550

* .92 : 1,426

Yep, that's just about what the bill they sent in the mail says!

"And your son's relatively high salary given his young age and relative inexperience is a large part of the reason why house prices have ballooned in this country and this town in particular."

ReplyDeleteWarren Buffett lives in Omaha. Housing prices must be really high there!

"The real question is why is Va_investor trolling the site?"

ReplyDeleteva_investor is not a troll. He is one of the people presenting the most well-thought-out arguments from the other side. The trolls here generally go by the name "anonymous."

Although I also wonder why serious housing bulls are interested in this site, a person's motive does not invalidate the logic of their arguments. Attacking someone's motive instead of disputing the logic of their arguments is a well-known logical fallacy.

-

ReplyDeletehere's a spreadsheet tool to help you find an entry point in a falling market -

http://www.files.bz/files/11251/RealEstateValuationMethods.xls

what do you think?

anon (4:56)

ReplyDeleteI've only taken a quick look at it (I plan to look more closely later), but where do you account for the value of the land? For example, a minimal value for a minimum sized lot in gentrified areas of DC would be something like $500,000 ... Your model isn't capturing that fixed cost ... or did I miss something?

VA Investor is not a troll. From his posts he appears to be a successful long term real estate investor and landlord.

ReplyDeleteKudos to that. It's a great position to be in.

He's generally bullish because he's smart enough to run his business to withstand RE cycles.

My $0.02.

I actually said trolling, I didnt mean he was a troll. I meant why is he actually here? If he knows we are wrong about the bubble why would he even be looking at sites like these? My first thought is that he suspects something might be wrong in the realestate market.

ReplyDeletebob

I am here because I like real estate alot. I have been into it since my early 20's. Used to read everything I could get my hands on.

ReplyDeleteI had a plan in my 20's to buy enough real estate by age 30 that I could justify not working and handling the RE full time.

I planned to have a large enough stream of rental income down the road to cover most of our retirement needs. I did this using present value and assuming rents would keep pace with inflation.

The final assumption is that all the properties would be paid for by retirement (55).

I always "make money going in". That way I can get out without a loss, if need be. There has never been a "need be".

There is alot of good info here so I like to visit often. I spend little time on the properties and this provides a hobby of sorts.

In 2008 or 09, I may be busier buying places. For now, I spend about an hour a day looking for a steal - mainly vacant land, as I don't want any more rentals.

There you have it. No trolling here - although I do sometimes enjoy a good "heated" discussion. David's delete button hampers this however.

It's David's blog, so he can do what he wants.

ReplyDeleteUnfortantely, he has nowhere near the readership and contributions as the Housing Bubble blog - now that's a quality blog, David.

I agree that the Housing Bubble blog is pretty good. The problem, for me, is that it is mainly left-coasters and I prefer a more regional perspective.

ReplyDeleteThe juxtaposition of Lereah's book's (released one year apart in February) have been noted on Wikipedia's entries for the US housing bubble and David Lereah.

ReplyDeletehttp://dcbubblemeter.blogspot.com

ReplyDeleteTo be fair to Lance, for most families owning a home over time is better than not owning a home. That said, overextending financially to buy into this bubble is insane. Chants of 'real estate never goes down', 'it's different this time', or my favorite, 'the real estate market HERE is different', offer little comfort for those trapped underwater for decades, bound to homes they no longer want by debt that exceeds what they can sell for, sometimes unable to sell even at a substantial loss.

ReplyDeleteThis bubble is a replay of the late 80's. I cringed when I read of people standing in line for days and fights breaking out to buy into the latest condo developments. Deja vu all over again.

The banks will be facing strick new rules regarding IO loans by the end of the summer. That will drain what's left of the wind that has created the current bubble. The bubble gentry, the paper rich who own several rental condos purchased in the last half decade, will suddenly face strong negative cash flows when faced with 'real' mortage payments. As YoY prices turn more negative, we'll see a panic rush toward the exits which will amplify the selling, just as irresponsible lending amplified the buying.

If someone is rich enough to pay cash and absorb the loss if they have to sell in the next ten years or so (which is about how long it took for prices to recover from the 80's bubble), then cool, do it. Pay the seller a bonus for good measure. And the relator, and banker, too.