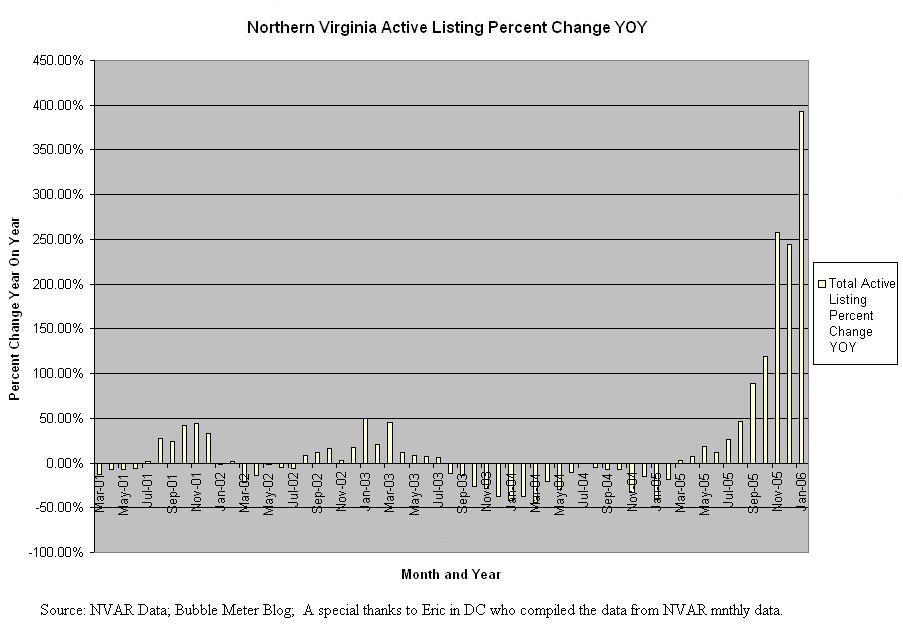

Active listings (inventory) are exploding in Northern Virginia as speculators and others want to sell properties. [click on image for larger version] "Inventory spiked last year with more than 7,000 active listings. For nine consecutive months in 2005, inventory in Northern Virginia increased compared to the previous year. The year ended with 5,659 active listings, 244 percent more homes on the market compared to December 2004. (The Connection, Feb 16)"

Meanwhile the number of sales per month continues to decline compared to last year's monthly sales.

Finally, the average price has peaked. Some would argue it is a seasonal effect. However, the number of active listings in January 2006 was 392% greater then January 2005. At the very same time the number of housing units sold in January 2006 was 29.6% less then in January 2005. Housing affordability remains at an all time low in the area. There will be no spring buying frenzy. Expect continued price declines in the Northern Virginia housing market.

A huge thanks to Eric in DC who compiled the numbers from the Northern Virginia Association of Realtors website.

Granted things are going down the toy-toy but showing these graphs this way as a percentage YOY is not the most honest way of portraying this data.

ReplyDeleteObviously there are lots of different ways to show the data. I will show it some other ways in teh future.

ReplyDelete"Granted things are going down the toy-toy but showing these graphs this way as a percentage YOY is not the most honest way of portraying this data."

Thats how the realtors love to show the data percentage YoY.

Well, those graphs and facts are one side of the argument. But what abou the other side? ;)

ReplyDeleteI'd like to see an intervie of someone that has chosen to buy a $400,000 condo at this time in this market. Like, what are they thinking?

ReplyDeleteAnyone know when the realtors will release the February numbers? It will be interesting see if we get a second decline (and thus, a "trend").

ReplyDeleteMan, there are so many new condos that will be completed in this area in the next six months. I think the single family house market will suffer but not implode -- there is such strong growth in this area -- but I suspect that condos may really take a hit.

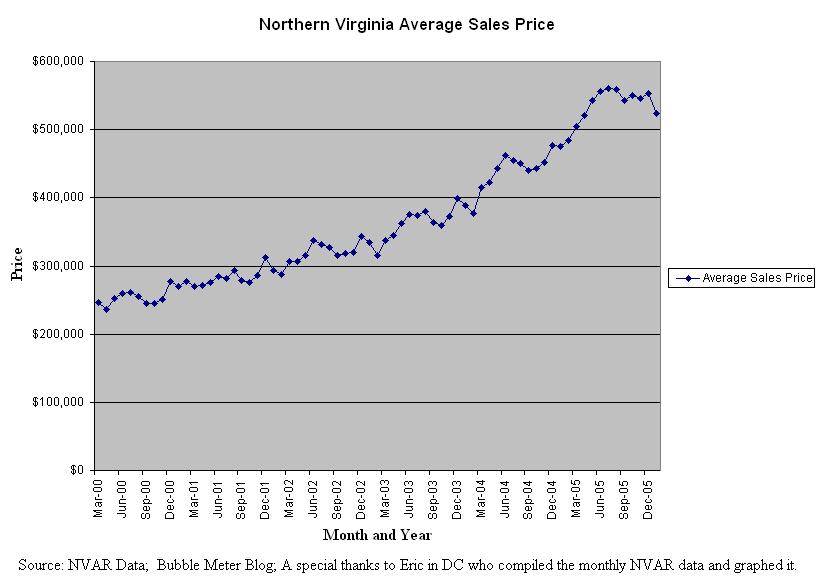

It looks like, from the historical pricing chart, if we get through April/May with flat or declining prices, then we will be able to confirm a real shift in market psychology.

ReplyDeleteIt would be nice to see a chart of real prices, not nominal.

No question condos will take the biggest hit. We won't see the biggest losses until 3Q and 4Q of 2006. That's because many new condo developments in their final construction stages all around the DC metro area. I think there are 40,000 condo units in the making around the DC area. That's a classic glut on the market.

ReplyDeletePeople who bought the condo conversions are going to get HAMMERED. They will drop like a rock in value. Savvy real estate hunters will look for TRUE condo developments.

If you own a single-family home, you should have no worries. You might have some price depreciation but not much. Sit tight and enjoy the house!

For you condo owners out there, may the force be with you.

David,

ReplyDeleteI live in Silver Spring, MD. Do you know if there is a local real estate association for suburban Maryland? I am curious about the MD real estate market since that is where I hope to buy some day.

http://www.mdrealtor.org/statistics.asp

ReplyDeletehttp://www.gcaar.com/default.htm

My Dad has a house in Dale City. About 4 or 5 similar houses were sold last fall in the $400,000 range. I go the sales data from zillow.

ReplyDeleteThere is no way those houses are worth $400,000 to your average home buyer.

The fed just released data on the American public. Americans don't save, they have barely any money invested in stocks, they are losing jobs to outsourcing. That leaves us with the question:

Where is the money going to come from to pay off all the debt created in the last 5 years?

I hear the Wal-mart is hiring greeters.

ReplyDeleteI disagree that SFH prices will be unaffected even if the condo market implodes. There are certainly buyers out there who would be willing to sacrifice the dream of buying a house and buy a condo on the cheap instead. So, if we see condo prices crater, condos will become somewhat more attractive vis-a-vis houses. This leads to lesser demand for houses, leading to a drop in prices. There's no way condo prices could drop by 30% and not drag SFH's along with them, at least to some degree.

ReplyDeleteThe median for single family homes is higher in 2005 than $400,000.

ReplyDelete"There's no way condo prices could drop by 30% and not drag SFH's along with them, at least to some degree."

ReplyDeleteI think everyone on this board would agree that the SFH and condo markets are connected. We'll find out this year just how close they are in the NoVA area. I think condos and SFHs at the top and bottom of the market are going to get hit the worst.

Compared to other markets, though, this area has great employment, income and population influx numbers, so there will some positives that should mitigate the price drops in higher quality properties. Also, the DC area -- even more than other cities -- is suffering from rapidly woorsening traffic problems (other cities presumably build new roads from time to time), so I think we'll see prices drop more quickly in the more distant counties and Arlington/Alexandria/maybe Fairfax counties should do better.

It is going to be interesting to see whether this actually happens, after expecting price drops for the past five years or so.

Yeah, I never understand why it is perfectly natural that prices go up 100-200%, but if you think that prices will fall 50%, you are a nut.

ReplyDelete"Don't forget about all the people that refinanced. If you have owned for 20 years, but took out a heloc and only left 10% equity in 2005 then you are still at -10% equity."

ReplyDeleteIf you owned a house for 20 years, you'd have been sitting on a PILE of equity. If you borrowed all that money, where the hell did it go???? If it's all gone, that's your own damn fault.

IMO, DC is one of the few safe areas in the country. I lived there for 8 years, and recently moved to Miami to semi-retire and get back to my hispanic roots.

ReplyDeleteI owned a home at a very upscale condo since around 2000 in Old Town. I sold it in 2 weeks this month. I got lucky looking at the listings, but if you buy a condo in a very upscale building it will always be in demand in DC. There are too many transient people from other countries who are scared to live in houses (cultural security issue) or from other major cities around the US (NY for example).

My 2 cents. I think the biggest thing is for people to remain patient. I watched the dot com bubble burst, and the people who were hurt were the people who invested in things they knew wouldn't be attractive logically 10 years later. Buy something you know will stand the test of time, and always be high quality and you'll be fine. If you bought something with aluminum siding 30 miles from DC, then you did yourself a disservice by holding it.

In my experience, you can take advantage of hot markets like the dot com period, and the housing market (even now)......but just make sure you buy something STABLE and something you would buy even without the craze.

So people in areas like Ballston, Arlington, Old Town Alexandria who have purchased homes in the upscale high rises in the past 2 years, you're fine. That's the most attractive area for most Europeans, South Americans and urbanites for the next 25 years. It's beautiful, pretty safe, pedestrian friendly, good transportation and just feels "upscale".

I honestly miss it quite a bit. I think this same logic applies anywhere you buy. Then again I'm saying this simply because I would never consider owning an actual home. To do that in my own country (Dominican Republic) is an invitation to be killed. Glass is just not enough to make me feel safe. Now being up 10 floors is. :-)

Visit I-Agent.Com Today!

ReplyDeleteI-Agent.com has revolutionized the way you buy a home! By combining online strategies with personal, customized service we are able to refund you up to 2% of the purchase price at settlement. Become part of our exciting new strategy and save thousands of dollars in commission fee's next time you buy or sell a home.