Subscribe to:

Post Comments (Atom)

Bubble Meter is a national housing bubble blog dedicated to tracking the continuing decline of the housing bubble throughout the USA. It is a long and slow decline. Housing prices were simply unsustainable. National housing bubble coverage. Please join in the discussion.

The Bubble Meter Philosophy

The best way to get the housing market thriving again is to drop prices to the point where supply equals demand. Home sellers might not like it, but it's good for buyers and it's great for Realtors.

For Realtors, the best way to make more money is to sell houses quickly, and the best way to sell houses quickly is to convince the seller to drop the price.

For Realtors, the best way to make more money is to sell houses quickly, and the best way to sell houses quickly is to convince the seller to drop the price.

My Other Blog

Housing Prices Since 1970

National Housing Sites

Regional Housing Sites

- Bay Area Real Estate Blog

- Boston Bubble

- Burbed (San Francisco)

- DC Home Prices

- Flippers in Trouble (Sacramento)

- Frankly Realty (Virginia)

- Greater Northern VA Housing Bubble Fallout

- Irvine Housing Blog

- New Jersey Real Estate Report

- Patrick.net (San Francisco)

- Portland Housing

- Proffesor Piggington (San Deigo)

- Sacramento Land(ing) Blog

- Seattle Bubble

- SoCal Real Estate Bubble Blog

- Socket Site (San Francisco)

- Vancouver Condo Info

Economic Sites

Iacono Research (ad)

When will inflation-adjusted DC-area housing prices return to pre-bubble levels?

Are housing prices about to experience a double-dip?

How should the U.S. government balance the budget? (Check all that apply.)

What is your political affiliation?

What sparked the housing bubble?

Is the recession over?

Who bears responsibility for the housing bubble? (Check all that apply.)

What is your living situation?

Was subprime lending a cause or an effect of the housing bubble?

Follow Bubble Meter

Bubble Meter Archive

-

▼

2006

(546)

-

▼

April

(55)

- 803 7th Street NE #1: Condo

- No Risk of Paying Too Much for a Condo?

- New National Association of Realtor's Blog

- Seller at Halstead at Dunn Loring Trying To Sell

- Easy Money at The Bank?

- David Lereah's Latest Quotes

- Ben Bernanke On Interest Rate Changes

- Ben Bernanke Speech

- Another Casualty of the Housing Bubble?

- Media Headlines Misleading on New Home Sales Data

- New Home Sales for March

- Bubblization

- Mortgage Interest Rate Watch

- The Big News in Existing Home Sales Report is the ...

- NAR Existing Home Sales Out

- Washington Post Express Quotes Bubble Meter

- New: Baltimore Housing Blog

- The Bean in Millennium Park

- Oil Prices and The Housing Market

- BubbleSphere Roundup

- Weekend Reports & Open Houses

- 1413 N MONROE ST Arlington, VA

- No Soft Landing

- Mention in the Washington Post

- Latest Promotion for the Mica Condos

- Prediction: Fed Interest Rates to 5.25% in June; E...

- BubbleSphere Roundup

- Housing Markets that are particularly Interesting

- Update: Seller Refuses to Lower Price

- On Vacation & Thank You

- National 5/1 ARM Rates Increasing

- Homeless Man Gets Five Fannie Mae Loans In Florida

- Bubblicious Bench Update

- Washington DC Active Listings Increase Dramatically

- In DC Proper Median and Average Price Decline Year...

- Immigration March in Washington, DC

- Lots of Rowhouses for Sale in Gentrified Neighborh...

- BubbleSphere Roundup

- Days on Market Increasing in Northern Virginia

- Major Breaking News: March Numbers for Northern Vi...

- Price Reduced At Parker Flats in DC

- The Ownership Society or Debtship Society ?

- Bubble Market Defined

- Main Points of Housing Bubble

- Live Housing Chat on WashingtonPost.com

- Biased PollingPoint Question

- China & Mortgage Debt

- ARM 5/1 Rates Going Up

- Mica Condos Update

- Lereah on February Pending Sales

- BubbleSphere Roundup

- Q & A Session on the US Economy

- Rowhouse for Sale in Canton

- Real Estate Book

- Tulips From Amsterdam

-

▼

April

(55)

Eric in DC,

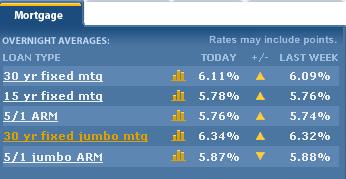

ReplyDeleteYou can't compare across different surveys. The Freddie Mac survey differs greatly from the Bankrate survey.

Not a problem, because it's not that the actual numbers are important, but the trend.

grim

Bankrate.com is a horrible place to find reality in mortgage rates.

ReplyDeleteI confess that I don't know where they get their numbers from, but I assure you it all has to do with the fact that they are a lead generation site. When someone clicks on these rates, they collect borrower information and sell it to mortgage lenders/brokers.

For this to work, you must have a rate that appears lower than the rest of the market.

The Freddie Mac site mentioned above is the best place to see where mortgage rates are really at. Then you won't feel like you were bait and switched.

Below is an article that I wrote about: The Truth about Online Mortgage Rates.

http://blog.pacesettermortgage.com/2005/11/the_truth_about.html

"Anyone going for an ARM now is reeeaalllyy stupid. They should get a 30 fixed an buy some points instead. "

ReplyDeleteWhy? The Fed has given hints that it doesn't intend to raise rates any further.

These rates are still, historically speaking, quite good. Those of you hoping for a market crash are probably going to be disappointed.

Everyone, take a look at one of today's headlines on CNN.com. prices have fallen back, but March sales are the highest they've been in over a decade.

ReplyDelete"New home sales soar. March gain of 13.8% the biggest in 13 years."

http://money.cnn.com/2006/04/26/news/economy/newhomes/index.htm?cnn=yes

Argh!

ReplyDelete...my faith is being shaken. When will this bubble pop?! I've been a "believer" for so long...four years

Just did my morning scan of about 20 economics/real bubble blogs and cannot believe that this sucker is still alive.

There are so many negative systemic risks looming (high oil, high interest, coming storm season, threat of Iran war...on and on). Couple that with the inevitable megatrends (US public/consumer debt, aging population, rising entitlement $ ...etc.)

I have rarely seen periods of time with so much risk AND a market willing to accept so little payment in exchange for assuming that risk.

wow!

"I have rarely seen periods of time with so much risk AND a market willing to accept so little payment in exchange for assuming that risk."

ReplyDeletewhat about the stock market crash of 2000? Could anyone justify those stock prices at the time? Some people were saying hey, this prices are totally insane, but if you were to believe them, you were considered a fool who was going to missing out on the biggest opportunity of your life.

Several of the trends mentioned have been around for awhile and while legitimate no silver bullet has been created to do away with them. Unfortunately it usually takes something to happen before people will do anything about it. Think about some of the major disasters that have gone in recent years, many times afterwords there are reports or other people usually warning others of what could happen yet nothing is done about it. (9/11, Katrina)

People in general seem to be reactive in nature, perhaps its because it is great visibility in recovering from adversity than there is in avoiding it (because you can never be sure how much you've done).

I think we are seeing what the economists call "loss aversion"

ReplyDeletethat is the tendency of people to avoid monetizing paper losses -- making them real

so the people who are underwater and who should sell don't -- keeping it 'unreal'

eventually, their hand is forced (you can only avoid the creditors' calls so long)

this sucker is going crack like a bull whip when it does

"Argh"

GRIM and Eric in DC.

ReplyDeleteYou are both right. The interest rates in the picture are actually very deceptive and low. Essentially, they are a compilation of rates that are doctored with points and "other fees", so the number is skewed lower ALWAYS. To get a more accurate picture, I recommend clicking on the "Interest rate roundoup" on the Bankrate site here:

http://www.bankrate.com/brm/static/rate-roundup.asp

I personally like to use ABN AMRO's website:

www.mortgage.com

Because they never put points into their calculations. Whenever you have multiple lenders compared, you will get the results skewed because they know people focus on rates, not points.

Anon "nyone going for an ARM now is reeeaalllyy stupid. They should get a 30 fixed an buy some points instead. "

ReplyDeleteWhy? The Fed has given hints that it doesn't intend to raise rates any further."

The Fed could stop tomorrow and long-term rates can still rise--look how long it took for them to really start rising after over a year of Fed hikes! They have some cathcing up to do, and it's ain't gonna be pretty...

Anon said "The Fed has given hints that it doesn't intend to raise rates any further."

ReplyDeleteThat may be true, but mortgage rates aren't closely tied to what the fed does. A better indicator of future mortgage rates would be the bond market.

"The Fed could stop tomorrow and long-term rates can still rise--look how long it took for them to really start rising after over a year of Fed hikes! They have some cathcing up to do, and it's ain't gonna be pretty... "

ReplyDeleteYou mean, you hope. Keep wishing harm to others. I'm sure that will only lead you to good things.

Keep an eye on the 10 year treasuries .... these strongly coorolate with mortgages .... Upward trend

ReplyDelete"The Fed could stop tomorrow and long-term rates can still rise--look how long it took for them to really start rising after over a year of Fed hikes! They have some cathcing up to do, and it's ain't gonna be pretty... "

ReplyDeleteYou mean, you hope. Keep wishing harm to others. I'm sure that will only lead you to good things.

Keep an eye on the 10 year treasuries .... these strongly coorolate with mortgages .... Upward trend

ReplyDeleteEveryone, take a look at one of today's headlines on CNN.com. prices have fallen back, but March sales are the highest they've been in over a decade.

ReplyDelete"New home sales soar. March gain of 13.8% the biggest in 13 years."

http://money.cnn.com/2006/04/26/news/economy/newhomes/index.htm?cnn=yes

Argh!

ReplyDelete...my faith is being shaken. When will this bubble pop?! I've been a "believer" for so long...four years

Just did my morning scan of about 20 economics/real bubble blogs and cannot believe that this sucker is still alive.

There are so many negative systemic risks looming (high oil, high interest, coming storm season, threat of Iran war...on and on). Couple that with the inevitable megatrends (US public/consumer debt, aging population, rising entitlement $ ...etc.)

I have rarely seen periods of time with so much risk AND a market willing to accept so little payment in exchange for assuming that risk.

wow!

Eric in DC,

ReplyDeleteYou can't compare across different surveys. The Freddie Mac survey differs greatly from the Bankrate survey.

Not a problem, because it's not that the actual numbers are important, but the trend.

grim